What Is The Difference Between An Authorized Member (AMBR) And A Manager In An LLC?

A Limited Liability Company (LLC) is a versatile legal entity for running a business. Since its relatively recent creation (Wyoming in 1977) it has quickly become an attractive option for real estate investors due to its tax flexibility and strong legal protections.

In practical business operations, many LLCs function either through a designated manager or the collaborative efforts of its members. Under the second model, an LLC may authorize members to make binding legal commitments for the LLC.

You may be wondering about the meaning of "AMBR." That stands for Authorized Member. This designation signifies an individual with the authority to make decisions and act on behalf of the LLC, including signing contracts and representing the business. An AMBR typically holds significant decision-making power within the company's structure

Whichever management framework is adopted, the details need to be outlined in the LLC Articles of Organization and the Operations Agreement. These two documents are the solid foundation of an effective LLC.

Authorized Members in An LLC

As we've said, an authorized member of an LLC is a member (or members) who are authorized by the governing documents to make binding legal commitments on behalf of the LLC. They include:

LLC Managers

A manager of an LLC is either a member or an outside party tasked with performing the day-to-day functions of managing the LLC. These duties are outlined in the LLC Operating Agreement.

Typically, the manager is given the power to perform the following for the company:

Make legal decisions for the LLC

Open and close business bank accounts

Buy and sell property e.g. real estate or financial instruments

Dispose of assets owned by the company

Obtain financing

Hire and manage LLC employees

An important note on LLC managers is that the LLC Manager is not liable for fraudulent statements for the LLC or the actions of any of the members of the LLC.

Basics of LLC Operations

Before you can understand the difference between an authorized member and a manager in an LLC, you should know the basics of LLC operations. In 2018 just under 200,000 LLCs were established in the state of Texas alone. The popularity of LLCs comes from its legal protections for owners, tax flexibility, and its less formal establishment process than traditional corporations.

As mentioned, a properly established LLC requires two foundational documents: Articles of Organization and the Operations Agreement. The first key step in how to start an LLC is filing the Articles of Organization with the state to outline the formation and purpose of the LLC. Governing the actual processes of the LLC, the Operations Agreement is important to ensure an efficiently run LLC and that it affords the most protections and benefits to its members.

The owner(s) of an LLC are referred to as its “members” and the default management is a democratic vote based on the ownership percentage. All the members enjoy protection from any liabilities taken on by the LLC and the LLC is in turn protected from any creditors of its members.

That said, it is imperative that the LLC Operations Agreement is drafted correctly as an ownership interest in an LLC is not automatically protected against personal creditors. If correctly drafted, however, the most a personal creditor of one of the members could obtain is the cash distributions that that member would have been entitled to.

LLC Articles of Organization and Operations Agreement

As one can imagine, an LLC that functions the best and provides a management structure sufficient for the purposes for which it was created will have well-drafted Articles of Organization (legally required to be filed with the state) and Operations Agreement (governing the functional processes of the LLC but not a legal requirement).

Particularly, these documents will contain provisions outlining the duties and privileges of the LLC’s authorized members and managers, if any.

Your LLC: Member Managed or Manager Managed?

Logically, there are only two options for how an LLC functions from a management perspective: democratically managed by the members or managed by an appointed manager. If it is member-managed then having an authorized member imbued with the power to enter the LLC into legal arrangements will often make practical sense.

Which One Is Right for You?

As a generalization, the larger the LLC the more practical it becomes to have a manager-managed model for the LLC. Aside from the practical advantages, the other key benefit from having a manager manage the LLC is to allow for passive member investors.

Many smaller LLCs prefer to manage the company as a team with, if needed, one or more members being authorized to sign on behalf of the LLC.

In either case, the key is getting the LLC Articles of Organization and Operations Agreement drafted correctly. With well-worded foundational documents, an LLC is an ideal flexible legal entity for conducting business.

The Fractional Family Office: Your Financial ‘Dream Team’

Like life itself, the most important thing in financial management is who you trust enough to accompany you on your journey.

That’s why a great team makes all the difference. But finding the right people can seem like an impossible task.

Who can help you save money with advanced tax strategies?

Who can help you grow your money with elite investments?

Who can help you keep your money safe using the legal structures it takes to protect everything you’ve worked for?

And even if you’re fortunate enough to find these unicorns, how do you know if they have your best interests at heart?

Billionaires do this by hiring a "Family Office,” a staff dedicated to building and protecting their wealth. They have attorneys, CPAs, coaches and a host of other specialized services watching their back at every turn.

Now here’s the good news: In 2025, the Family Office concept is available to those of us who aren’t billionaires. This means you can have vetted professionals on staff and a network of providers vetted to handle all of your tax and investing needs no matter who you are, where you're located, or what investing you're doing.

Let’s take a closer look.

Start With Your Executive Team

You need proactive guidance to achieve your financial goals. Chances are you’ve worked with financial advisors and accountants before, but the likelihood of them being truly proactive in their approach is low.

In cases like these, you are the one doing the research, looking into tax strategies, reading articles about estate planning ….

A good fractional Family Office will take this work off your shoulders.

You’ll start by putting a strategic level Certified Public Accountant (CPA) on your team, someone who has the skills to take your tax burden as low as 0-10%. This partnership will be key for your wealth plan to be successful. The right CPA is someone who can implement the right tax strategies for you and give you proactive advice about saving money by improving your tax strategy.

Next, you’re going to grow your money with elite investments. This means hiring a Chief Financial Officer (CFO) and plugging into a deal network. To achieve a target 20-30% ROI, first you're going to hire the CFO to help you model investments.

You also need access to a deal network of high performing investments. The CFO is going to talk to you about blended ROI. This isn't just normal ROI like your financial advisor would talk to you about. And it's not just tax savings like a regular CPA would talk to you about. This is both of those combined.

The CFO is also going to guide you on how to protect your income through tax shelters or tax advantaged investments.

Finally, your executive team will be rounded out with a chief legal officer, basically an asset protection attorney. This will help you keep your money through legal structures that protect your wealth. This person will identify all the risk factors that you might be exposed to and help you mitigate them. They do this by creating the right entity structure and by providing ongoing estate planning and maintenance.

A Fractional Family Office Can Keep You Compliant

It's important that you get the right structure in place before you make investments in non-traditional assets. For example, Royal Legal Solutions helps investors use an LLC that is 100% owned by your IRA to incorporate cryptocurrency into their retirement accounts. This gives your crypto investments you the same tax-advantaged status as the IRA.

If you don't have a LLC (limited liability company) and a Self-Directed IRA structure set up already, your Family Office team can help.

They will also review your investment options and business structures to ensure they are up-to-date, compliant, and bulletproof against whatever the future holds. The right team will help you to ensure ongoing compliance with your state and local laws and tax requirements.

Your ‘Dream Team’ should give you actionable steps to take, making sure your asset protection plans are up-to-date and your financial dreams are closer to becoming a reality.

Private Foundations: A Practical Guide To Tax Savings

Private foundations enjoy tax-exempt status, but they are still subject to unique and sometimes complex tax rules under the Internal Revenue Code (IRC). From filing requirements to avoiding costly penalties, here's a streamlined overview of what private foundations need to know.

Understanding Governance and Deductions

Private foundations are governed by strict rules not applicable to public charities. In addition to normal “fiduciary” duties, they face penalties, often in the form of taxes in these areas:

Self-dealing: Prohibited transactions between the foundation and “disqualified persons” such as major donors or trustees.

Excess business holdings: Foundations cannot own too much of a business enterprise.

Jeopardy investments: Investments that risk the foundation’s ability to carry out its mission.

Taxable expenditures: Payments not aligned with charitable purposes, such as political lobbying or unapproved grants.

Net investment income: A 1.39% tax on income such as dividends, interest, and capital gains.

Contributions to private foundations are tax-deductible but may be subject to limits (typically 30% of adjusted gross income for individuals).

Identifying Unrelated Business Income (UBI)

UBI arises when a foundation earns income from a trade or business that is regularly carried on and not substantially related to its exempt purpose. Passive income (e.g., dividends, royalties) is generally excluded—unless it’s debt-financed.

If UBI exceeds $1,000, the foundation must file Form 990-T. Tax is assessed at standard corporate rates, and estimated taxes may be required if expected liability exceeds $500.

Careful tracking of expenses related to UBI is critical for reducing tax liability. Expenses must be directly tied to the unrelated business and reasonably allocated.

Calculating the Net Investment Income Tax

Private foundations are subject to a 1.39% tax on net investment income. This includes:

Interest (except tax-exempt)

Dividends

Rents and royalties

Capital gains

Income from limited partnerships

Deductions may include necessary expenses incurred to generate or manage investment income. However, previously paid excise taxes cannot be deducted.

Meeting the Annual Distribution Requirement

Nonoperating foundations must distribute at least 5% of their average annual noncharitable-use assets. Qualifying distributions include grants to 501(c)(3) public charities and certain administrative expenses.

Failure to meet the minimum distribution requirement results in a 30% excise tax on undistributed income, with a 100% tax imposed on persistent shortfalls.

Maintaining Expenditure Responsibility

When making grants, especially to foreign or nonqualified organizations, a private foundation must follow IRS expenditure responsibility rules. This includes:

Conducting a pre-grant inquiry.

Establishing a written grant agreement.

Requiring periodic reports from the grantee.

Reporting to the IRS annually via Form 990-PF.

Investigating any misuse of funds.

Failure to comply may result in excise taxes and jeopardize the foundation’s tax-exempt status.

Recognizing Operating Foundations

Unlike nonoperating foundations, operating foundations directly conduct charitable activities. While they share many tax rules with nonoperating foundations, key distinctions include:

Donations qualify for higher charitable deduction limits (up to 60% of AGI).

They are exempt from annual distribution excise taxes.

They must meet both an income test and one of three operational tests (assets, endowment, or support) in three out of four years.

Operating foundations are less common and typically more complex to manage.

Avoiding Self-Dealing Pitfalls

Self-dealing rules prevent transactions between the foundation and disqualified persons. Common violations include:

Paying personal travel expenses.

Renting property from a family member.

Awarding scholarships to relatives.

Penalties include a 10% excise tax on the self-dealer and a 5% tax on any foundation manager who knowingly participated. If not corrected, second-tier penalties of up to 200% may apply.

Applying for Tax-Exempt Status and Filing Requirements

To qualify for exemption under IRC Section 501(c)(3), an organization must legally form as a nonprofit corporation or trust and include clauses in its governing documents that support a charitable purpose.

Once established, the foundation must apply to the IRS using Form 1023 or the simplified 1023-EZ. If the application is submitted within 27 months of formation, the organization will be treated as exempt retroactively from its formation date.

Annually, all private foundations—regardless of income or activity—must file IRS Form 990-PF. Failure to file on time can result in daily penalties.

Final Thoughts

Private foundations play a vital role in philanthropy but must navigate a landscape of regulatory requirements and potential tax pitfalls. Understanding these obligations—from filing and reporting to expenditure rules and excise taxes—is essential to maintaining tax-exempt status and fulfilling charitable missions effectively.

Does Your Real Estate Business Need An Employer Identification Number (EIN)?

Launching a new real estate business is an exciting and rewarding way to build your path to financial freedom.

However, as with any business, you have to pay taxes (womp womp).

And a primary way that state and federal governments keep track of what you owe in taxes is with identification numbers.

One of the first questions you'll encounter when registering your business involves your Employer Identification Number (EIN). In this article, we'll discuss what an EIN is and help you decide if you need to apply for one.

What is an EIN?

An Employer Identification Number—abbreviated on forms as EIN—is a nine-digit number that the IRS assigns and uses to identify businesses and individuals for taxation. An EIN is also known as a Federal Tax Identification Number.

As an individual taxpayer, you identify yourself with your Social Security Number (SSN). However, as the owner of most business entities, you need an EIN to apply for your business license and file your tax returns.

That's right; we said "most" business entities. If your real estate business is a sole proprietorship or single-member LLC, you can use your SSN to file your taxes.

On the other hand, the IRS requires your business to have an EIN if you do any of the following:

hire employees

operate your business as a corporation or a partnership

have a solo 401(k) or Keogh retirement plan

file for bankruptcy

buy or inherit an existing business and plan to operate it as a sole proprietorship

file alcohol, tobacco, and firearms; employment; or excise on your tax returns

withhold taxes on income (other than standard wages) paid to a non-U.S. resident

However, even if the IRS does not require your business to have EIN, many investors apply for one anyway.

Why? As you can see from the above list, having an EIN allows you to make more business moves than you are able to make as a sole proprietor. Some banks will even refuse to allow you to establish a business account or apply for business loans or credit cards without an EIN.

Some investors also feel that using an EIN can make your real estate business look more professional in business dealings. In a competitive real estate environment, an EIN can show that you take your new business seriously.

Also, using an EIN allows you to keep your SSN more secure from identity theft. For example, identity thieves can use stolen SSNs to file fraudulent tax returns. All business EINs are considered public information, but if someone looks for credit information, your EIN will be the only identification number they will find.

Does a general partnership need an EIN?

Although your general partnership may appear to be a simple agreement between two or more business partners, the IRS sees it as a separate business entity. Therefore, all partnerships—including general and limited partnerships—must have a separate tax identification number.

This requirement remains true even if your partnership has no employees. In addition, all partners must report their profits and losses on a Schedule K-1 when they file their personal income taxes.

Does a sole proprietorship need an EIN?

If you have a sole proprietorship with no employees, you may be able to file your business income taxes along with your personal tax return. You will use your SSN as your business taxpayer ID on your tax forms.

revise your LLC to be taxed as a corporation or S corporation

buy or inherit an existing business

begin bankruptcy procedures

How do you obtain an EIN?

Fortunately, unlike many aspects of launching a new real estate business, applying for an EIN is easy, and it's free.

The quickest way to apply online, using the IRS EIN Assistant tool. The process takes less than 10 minutes, and you will receive your new number immediately upon completion.

If you'd rather go the old-school route, you can download Form SS-4 and send it by U.S. mail to the IRS. The processing time for an EIN application received by mail is four to five weeks, according to the IRS website. Please note: The IRS warns business owners to beware of fraudulent online services that offer to apply for an EIN for you.

What if you already have an EIN?

If you already have an EIN and your business goes through some standard changes, you may be able to keep your old EIN. For example, if you change your business name or move to a different address, you can continue to use the same EIN.

However, you'll need to apply for a new number if the ownership or structure of your real estate business changes down the line.

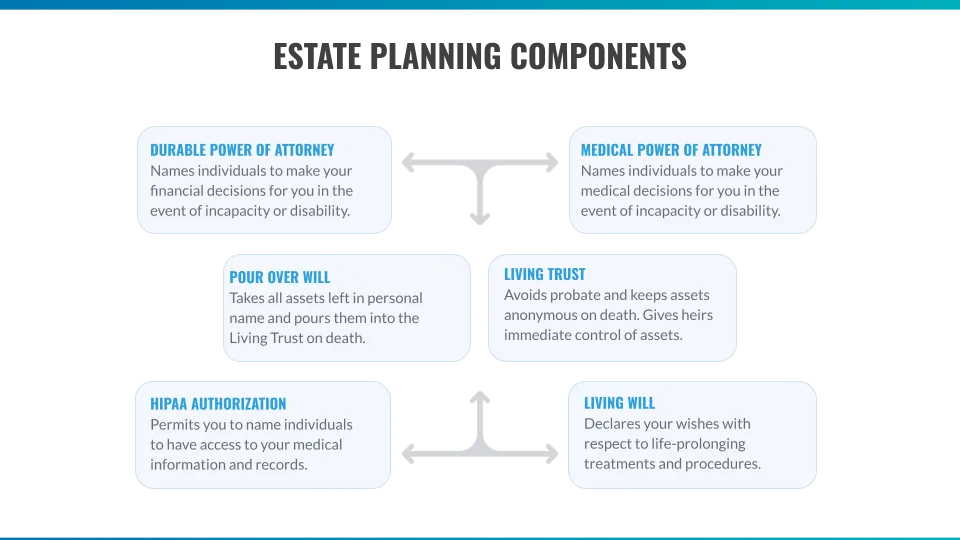

How To Protect Your Estate From A Predatory Remarriage

People tend to put off estate planning because no one likes to think about their own mortality.

That makes sense, but more than 60 percent of Americans don't even have a will in place, and you should not be among them.

Sure, the estate planning process means you have to focus on some unpleasant scenarios. One of them might be the thought of your spouse remarrying after your death.

Still, it is important to plan for your surviving spouse and consider the possibility that remarriage could put your assets at risk. Unfortunately, many unscrupulous individuals take advantage of widows and widowers. In this article, we will discuss how to protect your estate from a predatory remarriage.

How Can Your Spouse's Remarriage Harm Your Estate?

If you and your spouse have been married for many years and have children, you may have established reciprocal estate plans. Under these arrangements, a surviving spouse inherits all the assets of the spouse who passes away first. Then, the couple's combined assets go to their children after the surviving spouse's death.

You may have set up a bypass trust. A bypass trust is a legal arrangement with terms that allow a married couple to avoid or "bypass" paying estate tax on some assets after one spouse's death.

This process is straightforward unless the surviving spouse remarries. In that case, the new spouse may be able to become a legal heir to your surviving spouse's estate. This situation could threaten the assets that you intended for your children.

How Can You Protect Your Assets?

If you have a will that lays out your wishes for your estate's distribution, you may wonder why that document is not enough to protect your children. Unfortunately, a will cannot guarantee that your children will not be cut out of your estate if your spouse remarries.

None of us can predict the future, but careful estate planning is the best way you can protect your hard-earned assets and have the peace of mind that they will go to the people you love. A trust is a legal entity that allows a third party, known as the trustee, to hold your assets on the behalf of your beneficiaries.

Trusts can stipulate how and when your heirs receive your assets. A trust does not have to go through the lengthy and expensive legal process known as probate after your death.

What is A Family Wealth Trust?

A trust that is designed for estate planning for blended families is called a family wealth trust. A family wealth trust can be set up as part of a larger trust, or it can stand alone. Here are some of the key reasons why this solution will protect your children in the event you or your spouse have a predatory remarriage:

Your children are designated as the beneficiaries of the trust.

You can name your spouse, a close friend, or a legal or financial professional as the trustee.

Your surviving spouse can use or benefit from the property held in trust, but your children have full ownership of the property.

Only the trustee can sign checks for the trust and only for the purposes detailed in the trust. For example, if the surviving spouse is the trustee, the terms of the trust can prohibit the transfer of any of the trust assets to a new marriage partner.

A family wealth trust offers other protective measures against predatory remarriage. If your spouse remarries without a signed prenuptial agreement, they lose access to the property held in the trust. This step will encourage your surviving spouse to sign a prenuptial agreement, which is another essential shield against a predatory individual should the remarriage fail.

If you own considerable assets, here's another plus of creating a family wealth trust. This type of trust qualifies for the marital deduction in your gross estate. This qualification means that any of your assets that are above the applicable exclusion can go into the family wealth trust, allowing you to avoid estate taxes.

What Are Other Ways to Protect My Children's Inheritance?

As we said, estate planning leads you into some uncomfortable topics.

Here's another one. How can you make sure that your children do not squander their inheritance? This question may be weighing on your mind if you have a child that has problems with addictions or with failed relationships.

The answer to this dilemma is to create an investment tool called a spendthrift trust. A spendthrift trust places limits on a beneficiary's interest in the trust assets. Limitations might include paying only for your beneficiary's basic living expenses or making only limited payments directly to the beneficiary.

A spendthrift clause may be written to suit your individual circumstances. For example, the clause can include protection of the trust assets if your adult child goes through a divorce. In other words, it can offer your child protection from their own predatory marriage or remarriage.

With proper planning, your family wealth trust can be written to help your family for decades. For example, you can stipulate in your trust that your assets be passed down to your grandchildren rather than your son-in-law or daughter-in-law. Assuming your trustee manages your assets well, this means that your hard-earned assets will benefit your family for generations to come.

Every state varies in what they allow in terms of trust provisions. Your attorney can help you understand the rules in your state.

Finally, despite the word "wealth" in its title, a family wealth trust is not just for the very rich. If you have a moderate estate, your family can still benefit from this vital estate planning tool.

How Assumed Names Disguise Your Ownership (And Help Make You Lawsuit-Proof)

Your business may operate under an Assumed Name (also called a fictitious name, trade name, or doing business as (DBA).

An Assumed Name is simply any name other than your or your business's legal name.

Value of a DBA/Assumed Name

An "Assumed Name" can help you avoid potential legal pitfalls by giving you a "Doing Business As" name that is different from your company’s official name or personal legal name. It also allows you to have a business bank account even if you're a sole proprietor.

In Texas, we refer to DBA registration as filing an Assumed Name Certificate. Any type of entity structure can file an Assumed Name, whether you are operating as a sole proprietor, a partnership, a corporation, or an LLC.

Public Interest in Disclosure

Public interest in disclosure is the legal principle that a court should have access to relevant information, and that an opposing party (a litigant) should have access to all relevant information to make their case.

Legally speaking, your DBA is the public disclosure associated with the identity of the true party in interest (you) and the location where the party may be served with process (if suit is filed). Public interest in disclosure was created from the belief that is in the public interest to be able to ascertain whom to sue and where exactly the service of process can be performed.

What This Means If You Are Sued

What if your real estate business is taken to court? The potential plaintiffs will be able to benefit from your DBA filing requirements. Each and every day suits are filed against Assumed-Name defendants.

An attorney is probably going to be able to dismiss a suit that is filed against the Assumed Name (usually associated with a corporation or LLC that has a liability barrier). To have a better chance of winning the suit, the plaintiff should refile the case against the true party behind the DBA.

Note: It is not mandatory for a legal entity to have its business headquarters where you conduct business. In fact, requesting an out-of-county service of process gives your legal opponents additional delay and expense. However, this is when many plaintiffs will certainly give up.

What Laws Apply To Assumed Names?

An individual or company may possess as many DBAs as they desire, at the state or county level. A period of ten years can be covered with a single filing. A filing of a particular form may be used to terminate or abandon a DBA.

You should verity the county clerk's website within the county where you have your main headquarters or where you perform your services. Texans can visit the Secretary of State website and fill Form 503 for a state-level filing.

You are required to mention the counties where an Assumed Name will be used in this form. You need to check the box for “All” in case the entity will potentially use its Assumed Name in all counties in Texas.

A notarized DBA filing for people, companies and others is required by the Texas Business and Commerce Code chapter 71. You are required to state the psychical address (location) of your business. In case the county where the company has its main headquarter is different from the proposed county of business, you must file a DBA in both counties.

Let's imagine that you have a California LLC and wish to conduct business under an Assumed Name in Miami. Should you file an Assumed Name certificate in both counties? The answer is YES. Both the domestic and foreign entities within the scope of your business are included in the statute.

State vs. County Filing of DBAs

After you have formed an LLC, you need to get a DBA. However, where should the filing be performed, at the county clerk's office or with the Secretary of State?

The DBA needs to be filed as at both levels, according to the Business and Commerce Code:

"The corporation, limited partnership, limited liability partnership, limited liability Company, or foreign filing entity shall file the certificate in the office of the Secretary of State and in the office or offices of each county clerk as specified by Subsection (b) or (c)."

Even though filing with the Secretary of State is usually neglected by smaller entities who often file just in their local county, you need to consider that the statute says “and” when referring to state and county filings.

The county clerk needs to discover if a proposed DBA is available at the county level. The main thing to consider is that your proposed name should be different from another entity's filed Assumed Name that operates in that county. It is not mandatory to ascertain if a particular name is available, considering the fact that the DBA filing is essentially a notice filing. Simply file Form 503.

There are 254 counties in Texas. Is it important to file in the county where you live when you are obtaining a county-level Assumed Name for daily usage and banking purposes? The answer is no.

You can file for a DBA from El Paso County and the bank will still accept it, regardless if your are operating in Houston.

You should also consider the fact that there is no central data base connecting the Assumed Name records of Texas's 254 counties. You might want to get your company's DBA far from its true base of operations and in a county whose DBA database hasn't entered the online world yet, if asset protection/anonymity is your goal.

What About A Series LLC Doing Business through One of Its Series

Series are viewed as sub-companies, so an individual series has the power to sue and be sued; to contract; and to hold title to real and personal property, according to Business Organizations Code section 101.605.

However, the series has to function or hold title under its own name to fulfill these functions at the series level. This in turn demands that the series obtain an Assumed Name Certificate.

Are there any causes for this situation? Yes there are! First of all, technically speaking, the series is not an independent legal entity. And since it is running under an Assumed Name, is should possess a DBA on file. Additionally, the DBA filing should be conducted both at the state and county levels.

The name of the entity conducting business as an individual series will contain the basic Assumed Name for a Series LLC. As an example: “ABC LLC conducting business as ABD LLC-Series A.” Section 71.103 requires an Assumed Name filing both at the office of the Secretary of State and the county where Series A does business.

Can My Husband and I Own Our Business Together as a Sole Proprietorship?

There are some cases where a couple who run a business together wouldn’t be interested in creating a formal business entity.

The question then becomes: can that business, being run by a married couple, be considered a sole proprietorship?

The answer is yes. The IRS allows a lone exemption for married couples who want to structure their business as a sole proprietorship.

Before going into details on that, there are typically four different kinds of business structures that the IRS recognizes. Those include:

Sole proprietorships

Partnerships

Limited Liability Companies

Corporations

In order for the business you run with your spouse to qualify as a sole proprietorship, the following conditions must be met:

There must be no other employees actively engaged with the business. This includes children or other relatives.

Both spouses must materially participate in the running the business.

With those requirements met, each spouse would be required to file their own Schedule C, reporting their individual share (usually an even split) of the business’s income. Each spouse in the husband-and-wife business (sole proprietor or partnership or other) would also need to file a separate self-employment tax form.

Should My Spouse and I Run Our Business as a Sole Proprietorship?

This, of course, is a separate issue entirely. The big advantage of a sole proprietorship is that it’s one of the easiest business structures to establish. The major disadvantage of this structure is that you and your spouse are 100% liable if the business fails. Sole proprietorships offer no protection from creditors.

Another option that many married couples employ is a partnership. For tax purposes, it can be easier to file since there is only one form involved. On the other hand, the business will be required to obtain a tax identification number. Partnerships might also be subject to state and federal regulations. The major upside, however, is that partnerships offer more opportunities for growth.

There are no regulations that state that if you start a business as a joint venture LLC, which for tax purposes is considered a sole proprietorship, you cannot later change the structure of the business to a partnership, LLC, or anything else. For many married couples, having the option to start as a sole proprietorship affords them the opportunity to hit the ground running. It’s a simple and effective means of getting their business started without needing to file numerous petitions with state and federal agencies.

What makes sense for your business in the early days, however, may not make sense down the road.

3 Key Tax Benefits of Using an LLC Structure

Limited Liability Companies have many useful properties for investors. Most of my clients approach me about forming Traditional LLCs or Series LLCs for asset protection, but often are completely unaware of the potential tax benefits their entity may provide.

Today, let’s talk a bit about the tactics you can use to minimizing your tax liabilities. Specifically, we will be taking a closer look at the tax benefits of an LLC structure.

Tax Status Flexibility

One of the appealing tax benefits of LLCs is that you get to choose the manner in which it is taxed. But owners of Series LLCs don’t have to miss out on the fun. In fact, if you own a Series LLC, you can tax each Series differently if you desire. What exactly does that mean? Let’s take a closer look at how LLCs are taxed.

You may make your pick from any of the following three tax status elections when forming an LLC (or Series within a Series LLC):

Disregarded Entity. A pass-through entity, also commonly referred to as a flow-through entity allows taxes to be passed onto your personal tax return. Learn much more about the benefits of pass-through tax treatment for real estate investors from our previous article on the subject. Single-member LLCs and married couple LLCs are typically treated this way automatically in most jurisdictions.

Partnership. Partnership taxation is the default status of multi-member LLCs, but they may choose to change to S-Corporation or Disregarded Entity status. In entities taxed as partnerships, each member receives a Schedule K-1 and reports their share of the profits and losses. This information, along with a completed Form 1065 for partnership taxation, will be attached to members’ tax returns. In this way, the company isn’t billed, but the members each pay their fair share of the taxes.

S-Corporation. This status makes sense for anyone who would benefit from the lower tax rate on the entity’s first $75,000 in income. It’s treated more like a corporation, albeit with different provisions than the more complex C-Corporation. It also comes with a super sexy form called Form 8332. Filling it out might not be a blast, but the savings sure can be for certain investors.

Note that there is an exception to the flexibility norm. Single-member LLCs are more limited and may be forced to file as a sole proprietorship, then report income or losses on their personal returns. It is also important to be aware that the above are simply tax classifications rather than different types of entities. It can be easy to get the impression that an S-Corporation is an entity when indeed it is a tax status, as a C-Corporation is an entity.

Which tax option will be best for you? As with most answers in the financial realm, you’ll find that it depends on your individual circumstances, status, and ambitions in the real estate business. Only a qualified attorney and CPA should be trusted to give tax advice.

Deductions and Credits Galore For Those Willing to Look

If you’re serious about lowering your tax bill you know the power of deductions. So we recommend that you deduct, deduct, deduct everything that you can. No business expense is too small or inexpensive. See if you qualify for fuel deductions, and take a good written record of everything you really need for work and its cost. It may seem silly if you’re looking at many small receipts or expenses, but the old adage about how they tend to add up is true.

The fact that you may not be aware of deduction and credit opportunities is yet another good reason to have a solid CPA and attorney on your real estate dream team. These pros will often point out savings options you didn’t even know you were missing out on. So go forth and deduct shamelessly. It’s a win-win for both client and CPA.

Personal Assets May Be Leased to the LLC

If a valuable assets drag you into a higher tax bracket, an LLC offers a handysolution. You may be able to minimize this situation by leasing the asset to yourself (specifically, your LLC) with a formal leasing agreement. Such arrangements lower taxable income and often allow for deductions.

For example, a home office is an item you lean on come Tax Season when you’re deduction hunting. Learn more details about the home office deduction and who can qualify from our previous educational resource on the subject. Home offices may not only be deducted from your taxes, but also leased back to your LLC. When that leasing agreement goes through, you can write it off and claim it as a business expense. The fact that this type of business expense

Optimize Your LLC Tax Strategy With The Pros at Royal Legal Solutions

Between the asset protection and tax benefits, LLCs may begin to seem like a no-brainer. But to get the right entity that will do the best possible job for you, you may need Our crack team of attorneys and the CPAs we work with can assist you through any tax concerns you may have. As investors ourselves, we may have some more tips that you haven’t yet learned to exploit. Which ones will apply to you will depend on your personal circumstances.

If you are wondering how Royal Legal Solutions can help you save on your taxes, our consultants are happy to explain your options to you, answer your questions, and when you’re ready, set up your personalized consultation. We look forward to helping you keep more of your income where it belongs: in your bank account.

Find out about the tax savings strategies that you can implement as a real estate investor or entrepreneur by taking our Tax Discovery quiz. We'll use this information to prepare to have a productive conversation. At the end of the quiz, you'll have an opportunity to schedule your consultation. TAKE THE TAX DISCOVERY QUIZ

Is The Owner Of An LLC Public Record? Which States Allow Anonymous LLCs, Anyway?

Real estate investors love the liability and asset protection offered by a Limited Liability Company (LLC). Do you know what makes an LLC even better? When it's completely anonymous. Fortunately, some states offer you the chance to escape from unnecessary legal liability in the form of an “anonymous” LLC.

An anonymous LLC protects your privacy and keeps your ownership of the company out of the public record, which gives you more flexibility and security in managing your real estate investments.

If you're intrigued, keep reading. We'll explain everything you need to know about how to hide ownership of a company using an anonymous LLC.

Is the Owner of an LLC Public Record?

Whenever you start a new LLC, you have to file formation documents with a state government entity, often the Secretary of State. In most states, you have to provide the name of the person or entity forming the LLC and a registered agent. The registered agent is the person or entity responsible for receiving legal service and other essential notices on behalf of the LLC. Some states will also require you to list the LLC's manager on the formation documents.

When you file your LLCs formation documents, they become part of the public record, and anyone can access this information. If you'd prefer to keep this information private, there are several methods you can use to form an anonymous LLC.

Benefits Of Anonymity

With an anonymous LLC, sometimes referred to as a private LLC, the company's owners are not publicly listed in state records, as they would be with a regular LLC. Keeping things anonymous offers a variety of benefits to you and your company. We've listed some of the most valuable advantages of LLC anonymity below.

Maintaining Confidentiality

Starting an anonymous LLC to hold your real estate investments can help you keep your properties and financial status out of the public eye.

Protecting Privacy

Forming an anonymous LLC allows you to protect your privacy by keeping your name and address off the internet.

Preventing Harassment

If you keep your identity and address anonymous, you can avoid unwanted harassment from salespeople, competitors, or anyone else who is interested in you or the properties you own.

Frivolous Lawsuit Prevention

The world is full of "professional plaintiffs" and other opportunists who are looking to make a quick buck. Keeping your name off the ownership records for your LLC can help you avoid frivolous lawsuits.

Asset Protection

Holding your real estate investments in an anonymous LLC can help you shield them from lawsuits and your personal creditors.

How Does An Anonymous LLC Work?

There are a handful of methods you can use to create an anonymous LLC. The easiest way to do it is to select a state that allows you to incorporate anonymously.

The following states will let you create an LLC without making your name public record:

Delaware

Nevada

New Mexico

Wyoming

Establishing an anonymous LLC in any of these states lets you keep your name off the LLC's records. Which state you should choose for your LLC depends on what benefit is most important to you.

We've listed the most significant small business benefits offered by three of the most popular states below.

New Mexico

New Mexico is the only state that allows you to form an LLC without disclosing the members' names to the government, making it the option that offers the most privacy.

Delaware

Delaware is well known for its business-friendly laws and doesn't require corporate income tax. You'll only have to pay a $300 franchise tax each year.

Wyoming

Wyoming is one of the most tax-friendly states for anonymous LLCs, with no corporate income tax and annual fees as low as $50.

Forming An Anonymous LLC In Other States

If you want to create an anonymous LLC but don't want to start it in Delaware, Nevada, New Mexico, or Wyoming, you're not out of luck. Property owners can form an anonymous LLC in other states; there are just a few extra steps involved.

First, start an anonymous "holding company" in Delaware, Nevada, New Mexico, or Wyoming. A holding company is a business entity that is created to own other businesses and hold assets. Holding companies usually don't conduct independent business operations; they just profit from the companies and investments they own.

Once you've created your anonymous holding company, you can start an anonymous LLC in any state by simply listing the holding company as the owner. Since no records tie you to the LLC and no records connect you to the anonymous holding company, your ownership interest in the LLC remains private.

Should I Form My LLC Anonymously?

If you're looking to protect your privacy and keep your ownership information out of the public record, the answer is a resounding “YES!” Forming an anonymous LLC will allow you to guard your personal information while shielding your investments from creditors, lawsuits, and harassers.

How To Set Up a Land Trust For Each Investment Property You Own

Setting up land trusts for each investment property you own is essential. One benefit of the land trust is to keep ownership of the property private. This way, the land title office can no longer let the whole world know that you own the property. Many people can enjoy privacy of ownership and do so for a few different reasons. The benefits are below:

You can keep ownership of one or more properties private.

You have the ability to transfer ownership of one or more properties to someone else easily.

You can avoid probate on one or more properties you own.

You can have many owners of one or more piece of property.

The owner keeps tax advantage.

Land Trusts Can Help Avoid Moving the Investment Property Title To and From More Than One Name

Although the above five benefits are the main reasons for setting up land trusts for each of your investment properties, doing so can help in other ways as well. One way setting up a land trust for each of your investment properties can help the owner is by avoiding "churning" of the title. Churning means that the title goes through many different hands in a short time period.

The thing about the title going from one hand to the next and the next and so on is that a lender will not think twice about denying lending money for the property. This is because they may think thatthe title is going through many different hands really fast so as to make the investment property look like it is worth a lot more than it really is. This is why it is good to set up a land trust for your properties.

How to Set Up Land Trusts for Multiple Investment Properties

You can create land trusts for multiple properties by using two legal documents. Before you start with the documents, first you need to decide the name you are going to be using for your properties. Once you find a trusted friend or family member, you then see a land trust attorney who will draw up a contract that states what is happening and the rights of both parties, you and your land trust.

Once you both look over this document and you both sign it, you then need to record the trustee deed. However, once these two steps are done, the world will no longer be told that you own any of the investment properties you own. Once this is done, you can enjoy all of the benefits mentioned above of using a land trust for each investment property you own.

Find Out if a Land Trust is Legal in Your State

For years now, I’ve been telling people to use land trusts for their real estate investments. Not only does it provide protection from creditors but it also prevents them from using the Uniform Fraudulent Conveyance Act to access your assets. It’s also a great way to discourage would-be litigators from suing you since your name never appears on record that you own anything.

I’ve been talking about the importance of using land trusts for years now. One of the questions I keep getting is: Which "land trust states" will recognize this legal entity?

What States Allow Land Trusts?

Only six states have a land trust statute on the books. These states include:

Indiana

South Dakota

Florida

Hawaii

Virginia

Illinois

This doesn’t mean that you can’t form a land trust if you don’t live in these states. Most states without the legal structures in place defer to the Illinois Land Trust statutes to determine validity and case law. Apart from Louisiana, you can hold land in trust in any of the other 49 states and the District of Columbia. This has to be done in accordance with the law of any of the foregoing states given that the beneficiary, trustee, or the property is based there. The states of California, Colorado, Missouri, and Nevada have trust laws that allow trustees to hold title to property for a NAMED TRUST (note that it’s just a trust, not a land trust).

With the guidance of a knowledgeable lawyer, you can actually form a land trust in most states, even in Louisiana. The state still has the old French Civil Laws that will need an expert to navigate. One of the hurdles you might have is getting a good attorney in your state who’s well versed in land trust matters.

How to Go About Setting Up the Land Trust

To start setting up your land trust, deed the piece of property you’re buying to a friendly nominee. Should you run into problems down the road where the title company rejects your land trust, they will be able to recognize the last person in the title – the nominee. Thereafter, direct your nominee to sign a deed directly to your new purchaser. But there’s a catch to this approach – you need to be certain that your nominee will be around for the long haul. This is why you might want to consider a appointing close friend of family member as the nominee.

To avoid problems in future, you might want to have the grantor execute two deeds – one for the land trust (using trust deed language) and the other directly to the grantee. The deed to the grantee is a failsafe to be used if the land trust is found to be defective by your state law.

Personal Property Trust Vs Living Trusts & Land Trusts: Discover An Overlooked Asset Protection Tool

land trust vs living trust

personal property trust

Asset protection is a crucial component of financial planning for any real estate investor.

I've written again and again and again and again about the many tools you can use to keep your property out of the clutches of creditors and would-be-litigants (and new clients are always asking about the difference between land trusts and living trusts and personal property trusts).

While Land Trusts, Series LLCs, and anonymous trusts are some of my favorite tried-and-true asset protection methods, a financial planning tool that doesn’t get as much attention as it should is the personal property trust.

With this article, we're going to change that!

What Is A Personal Property Trust?

In general, a trust is a type of legal arrangement where a trustee holds title to specific property and manages it for the benefit of the trust’s beneficiaries. Trusts can be revocable, which means the trust can be altered or canceled at any time while the person establishing the trust is still alive. They can also be irrevocable, which means they cannot be modified or revoked.

Like a Land Trust or living trust, a personal property trust is a type of revocable trust. Whereas the Land Trust is used to hold real property, the personal property trust is used to hold title to personal property assets such as vehicles, boats and mobile homes.

Whenever an asset needs to be registered and included in public records, you can use a personal property trust to keep your ownership information private.

Since trustees must manage the trust assets as directed by the trust instrument, you can use a trust to transfer legal ownership and protect your identity while essentially maintaining complete control over the trust property. Generally, the sale of trust property requires approval from the beneficial owner, and the trustee cannot make the decision alone. Naming yourself as the beneficiary of a personal property trust can keep you in control of your assets.

What Are The Benefits Of Putting Your Property In A Trust?

The primary benefit of using a personal property trust is privacy. When you place your assets in a personal property trust, public record registrations will show the trust as the owner instead of listing your name. If you choose a privacy-protecting name for your trust, there will be no indications in the public record that you own the property.

A few additional benefits of using a personal property trust include:

Protecting your assets from lawsuits and other creditors

Avoiding the expensive probate process when leaving assets to trust beneficiaries

Flexibility in the types of personal property that can be placed in a personal property trust

The ability to retain control over trust property

The option to add and remove property from the trust

When Should You Use a Personal Property Trust?

As a real estate investor, there are several ways you can take advantage of the protections offered by a personal property trust. Here are a few of the most beneficial ways to use personal property trusts to help keep your real estate investments safe and private.

Mortgages

One of the most common uses of personal property trusts is to hold mortgages, since the ownership information for this type of asset can be found through a public records search. As a real estate investor, you may want to consider creating a separate personal property trust for each property for which you have a mortgage. This strategy will allow you to keep your ownership information private and avoid links between your various properties.

LLCs

Savvy real estate investors often use an LLC to own real estate directly or name an LLC as the beneficiary of a Land Trust. To add another layer of separation and anonymity to your asset protection strategy, you can use a personal property trust to hold your membership interest in the LLC.

If you use an LLC as part of your real estate asset protection plan, it’s important to remember that, in most states, LLC membership is included as part of the public record. One way to keep your LLC interests private is to list a personal property trust as the LLC member and name yourself as the trust beneficiary.

Vehicles

Any vehicle—including cars, trucks, and motor homes—that must be registered with the Department of Motor Vehicles is generally part of the public record, which can make your personal data open to public search.

You can avoid this by titling your automobiles to a personal property trust.

Given its various uses, a personal property trust can be a valuable tool for real estate investors, as well as people who haven’t caught the real estate bug (yet). No matter how you use your personal property trust, it is a practical but often-overlooked component of a successful asset protection plan. When deciding what financial planning tools are best for your real estate investment plan, it’s vital that you seek the input of an experienced asset protection attorney.

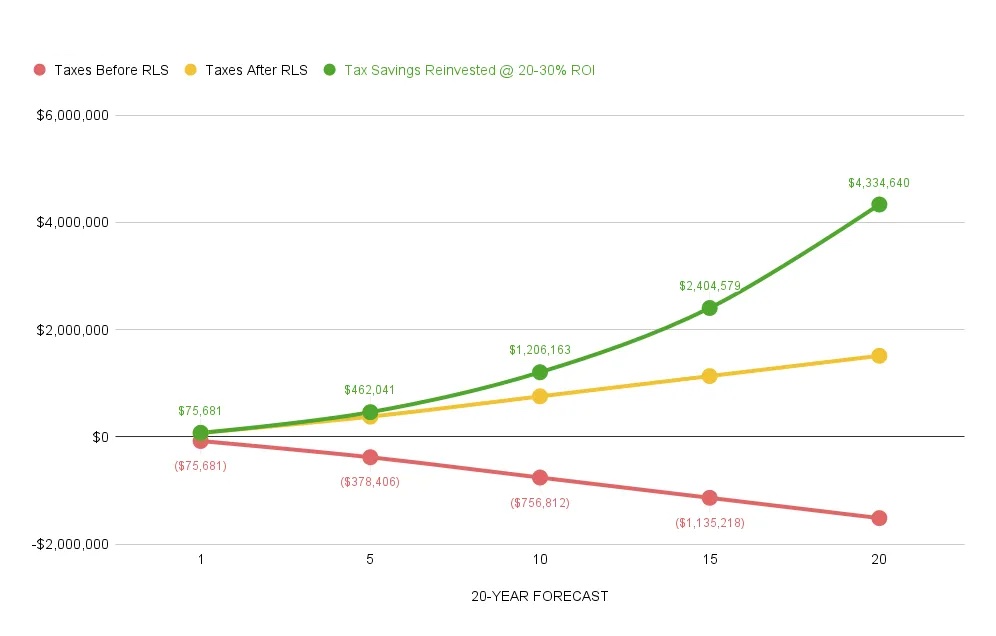

Short-Term Rental Cost Segregation Study Helps With 2025 Taxes

Rental Property Depreciation is a killer strategy for reducing taxes.

And short-term-rental (STR) owners need a cost segregation study to reclassify parts of their property from a standard 39-year life to shorter lifespans (say, 5 or 15 years.)

Even as bonus depreciation phases out to 0 percent by 2027, a cost segregation study can still maximize your property’s depreciation benefits.

Let’s take a closer look.

How to Use Rental Property Depreciation to Your Advantage

Rental property depreciation can be a game-changer when it comes to reducing taxes for your short-term rental (STR) business. And if you’re looking to deepen your role in the real estate industry beyond investing, learning how to become a real estate agent can open new professional opportunities while complementing your investment strategies.

By leveraging strategies like accelerated depreciation, you can take larger deductions in the early years of owning a property, freeing up cash flow and lowering your tax bill. Here’s how it works and why it’s worth considering.

What Is Accelerated Depreciation?

Accelerated depreciation allows assets to lose value more quickly in the earlier years of ownership, rather than spreading the deductions evenly over the property’s lifespan.

Why does this matter?

Bigger tax savings earlier on: You can claim larger deductions in the first few years the property is in service.

Lower taxable income: Reducing your reported profit means you may qualify for a lower tax bracket.

Improved cash flow: With a lower tax bill, you can reinvest savings into your business or other opportunities.

How Does A Cost Segregation Study Fit In?

The IRS typically allows residential rental properties to depreciate over 27.5 years and commercial properties over 39 years. However, not every part of a property needs to follow this timeline.

Look at it this way. When you buy or construct a property, it includes more than just the building itself. Think about:

Plumbing fixtures

Carpeting

Sidewalks

Fencing

If purchased separately, these items could be depreciated over 5, 7, or 15 years. A cost segregation study helps identify these shorter-life assets and accelerates their depreciation, giving you more tax savings upfront.

How Does a Cost Segregation Study Work?

A cost segregation study breaks down the purchase price or construction cost of your property into categories with different depreciation schedules. Here’s the process:

Identify short-life components: Examples include electrical outlets for appliances (5 years) or landscaping improvements (15 years).

Reallocate costs: On average, 20-40% of a property’s components can qualify for accelerated depreciation.

Calculate tax savings: By writing off these assets sooner, you significantly reduce your taxable income in the early years.

What’s Involved in a Cost Segregation Study?

A high-quality cost segregation study includes:

Review of property records: Cost details, blueprints, and other documentation.

On-site inspection: To identify and assess qualifying components.

Comprehensive reporting: Detailed findings with a breakdown of depreciation categories. If records are incomplete, professionals can still estimate values based on the property inspection.

When Should You Conduct a Cost Segregation Study?

Timing matters!

Best time: The year a property is purchased, remodeled, or constructed.

Planning ahead: If you’re building or renovating, consider a study before finalizing the infrastructure. For STR investors, acting early ensures you maximize your deductions as soon as the property is in service.

How Much Can You Save?

Let’s crunch the numbers with an example:

Imagine you own a short-term rental valued at $800,000.

Without cost segregation:

Depreciate over 39 years: $20,512 per year

Tax savings (at 37% rate): About $4,600/year

With cost segregation:

$100,000 of electrical fixtures (5 years)

$100,000 of plumbing fixtures (7 years)

$100,000 for parking, landscaping and storm sewers (15 years)

Now, instead of a flat $800,000 depreciating over 39 years, you allocate $300,000 for accelerated depreciation. This leads to significantly larger tax savings in the first year and beyond.

DIY Cost Segregation Studies—Are They Worth It?

While you can identify some short-life assets on your own, working with a tax professional ensures you get the full benefit of a cost segregation study.

There are two main approaches:

“Rule of thumb” method: Estimates based on similar properties; less reliable and higher risk.

Engineering approach: A detailed review using actual cost records; more accurate and preferred by the IRS. A professional specializing in cost segregation will typically use the engineering approach, reducing your audit risk and maximizing your tax savings.

Bonus Depreciation is Phasing Out: Act Now to Maximize Savings

Rental property depreciation, especially when paired with a cost segregation study, is a powerful tool for STR investors. By accelerating depreciation on certain components, you can:

Free up cash flow

Lower your taxable income

Reap significant tax savings in the early years of ownership

As the saying goes, all good things must come to an end. Under current law, bonus depreciation is being phased out:

2024: Reduced to 60%

2025: Drops to 40%

2026: Down to 20%

2027 and beyond: Completely eliminated (0%)

If you’re an investor looking to take advantage of this tax-saving strategy, now is the time. The sooner you act, the greater your potential savings before bonus depreciation disappears entirely.

Want to unlock these benefits? Reach out to a tax professional to see if a cost segregation study is right for your property. The savings could be substantial, so don’t miss this window of opportunity to optimize your cash flow and reduce your tax burden!

BONUS: 12 Common Questions About Cost Segregation Studies

1. What Is a Cost Segregation Study?

Every property is made up of a variety of assets, and each one has a different expected useful life. For instance, tile flooring is much more durable than carpet, right?

Tax law accounts for these differences and guides how capital expenditures should be depreciated. Using the Modified Asset Cost Recovery System (MACRS):

Residential real property is typically depreciated over 27.5 years.

Nonresidential real property is depreciated over 39 years.

Without a cost segregation study, all assets in a property would default to these timelines, even though it doesn’t make sense for shorter-lived components like carpet. Cost segregation adjusts this, giving you more accurate depreciation timelines—and better tax savings.

2. How Are Building Assets Categorized for Depreciation?

A cost segregation study breaks down a property into individual components, assigns costs to each using IRS-approved pricing guides, and places them into different categories based on their depreciation timelines. Here are some common categories:

15-Year Assets: Land improvements like parking lots, landscaping, drainage systems, outdoor pools, and sidewalks. By moving these assets into shorter-lived categories, they depreciate faster, which means more tax savings upfront and better cash flow.

3. Is Cost Segregation Worth It For Rental Property Investors?

Yes, cost segregation can offer a significant return on investment! While the cost of the study depends on the size and complexity of the property, the benefits often far outweigh the expense. Beyond accelerated depreciation, cost segregation can:

Provide data for future tax strategies.

Be updated if new tax laws or opportunities arise. To get a clearer picture of potential savings, many providers offer free estimates after reviewing your property details.

4. What Types of Real Estate Qualify for Cost Segregation?

Cost segregation isn’t just for office buildings or hotels—it can be applied to nearly all types of commercial and residential real estate, including short-term rentals. Popular property types include:

Garden-style apartment complexes

Manufacturing facilities

Auto dealerships

Self-storage facilities

5. Does Cost Segregation Create New Deductions?

No, cost segregation doesn’t create new deductions. Instead, it accelerates existing deductions by shifting them to earlier years of ownership. This lets you take advantage of the time value of money by getting tax savings sooner.

6. Can I Do a Cost Segregation Study Myself?

While cost segregation may seem straightforward, a quality study requires expertise. A professional will conduct a detailed forensic analysis of the property, breaking out assets, assigning costs, and ensuring compliance with IRS rules. This level of precision is key to maximizing your tax savings and minimizing audit risks.

7. When Is the Best Time to Perform a Cost Segregation Study?

The best time to perform a cost segregation study is right after a property is purchased or constructed. This ensures the study accurately reflects the assets in place when the property is first put into service, maximizing your tax benefits from day one.

8. How Far Back Can You Do a Cost Segregation Study?

You can conduct a “look-back” cost segregation study for properties purchased in previous years. This allows you to claim missed depreciation without amending past tax returns by filing Form 3115 to catch up on deductions.

9. Can Cost Segregation Studies Be Used as a Planning Tool?

Absolutely! Cost segregation can be integrated into your tax planning strategy before a property is purchased or constructed. For example, you can:

Design buildouts to maximize assets eligible for accelerated depreciation.

Incorporate energy-efficient features to qualify for additional credits like IRC Sec. 179D or Sec. 45L.

Align depreciation deductions with cash flow needs. The data from a cost segregation study can also set you up for future tax benefits, such as partial asset dispositions or tracking capital improvements.

10. How Does Bonus Depreciation Relate to Cost Segregation?

Bonus depreciation allows you to take an additional write-off for assets with a class life of less than 20 years. It’s a powerful tool that complements cost segregation, as the study identifies assets eligible for bonus depreciation. Under the Tax Cuts and Jobs Act, the bonus depreciation rate was 100% for assets placed in service between 2017 and 2022. This rate dropped to 80% in 2023 and will phase out entirely by 2027. Despite the reduction, cost segregation still provides significant tax benefits.

11. Is Cost Segregation Useful for Renovation Projects?

Yes! While cost segregation is commonly used for newly purchased or constructed properties, it’s also valuable for properties undergoing major renovations. By quantifying and categorizing assets before they’re retired, you can take advantage of the partial asset disposition (PAD) election to write off the remaining value of disposed assets. Renovated assets classified as Qualified Improvement Property (QIP) may also qualify for accelerated depreciation or bonus depreciation.

12. What Is Qualified Improvement Property (QIP) and How Is It Connected to Cost Segregation?

QIP refers to interior improvements made to nonresidential buildings after they’ve been placed in service, excluding structural changes, expansions, or upgrades like elevators. Thanks to the CARES Act, QIP now has a 15-year recovery period, making it eligible for bonus depreciation. Cost segregation helps identify and categorize QIP assets, ensuring they are accurately valued for depreciation purposes. This is especially beneficial for landlords providing tenant buildout allowances, allowing for faster tax savings on these investments.

Deductions for 2025 (Tax Year 2024): A Beginner's Guide

You’ve worked hard to get where you are, and one thing you’ve no doubt learned along the way is that tax season is usually the biggest pain when you’re managing your accounts.

And if you’re not familiar with the deductions you may qualify for that pain is even worse.

Don’t pull your hair out over the confusing (and ever-changing) tax code— just need some help from the right advisors. Then you can lower your overall tax bill and keep more of your hard-earned money.

In this guide, we’ll break down the essentials of tax deductions for tax year 2024 (what you’ll file in 2025). Whether you’re an individual filer, a small business owner, or someone looking to maximize advanced tax-saving strategies, this article will provide you with the tools you need to take control of your taxes.

We’ll start with standard deductions, the simplest way to lower your taxable income. Then, we’ll explore business deductions, which can help entrepreneurs and freelancers save big. Finally, we’ll dive into advanced deductions, perfect for those looking to optimize their finances with more complex tax strategies.

Let’s get started on your path to smarter tax filing in 2025!

Standard Deductions

As usual, taxpayers, including business owners, can choose between standard deductions and itemized deductions when filing their 2024 income taxes.

(The standard deduction or itemized deductions differ from self-employed business expense deductions. To maximize your deductions across all income types, we highly recommend you get the tax advice you need for your specific situation.)

Many prefer the standard deduction offered by the IRS due to its simplicity. This fixed amount reduces taxable income and varies based on your filing status. The IRS has increased the standard deduction to account for annual inflation. The standard deduction for married couples filing jointly for tax year 2024 rose to $29,200, an increase of $1,500 from tax year 2023.

For single taxpayers and married individuals filing separately, the standard deduction rises to $14,600, an increase of $750 from 2023. For heads of households, the standard deduction is $21,900, an increase of $1,100.

The standard deduction amounts for tax year 2024 (taxes filed in 2025) and for tax year 2025 (taxes filed in 2026) are as follows:

Filing status

2024 standard deduction

2025 standard deduction

Single

$14,600

$15,000

Head of household

$21,900

$22,500

Married filing jointly

$29,200

$30,000

Married filing separately

$14,600

$15,000

Business Deductions

The more tax deductions your business claims, the lower your taxable profit—and that means more money in your pocket.

But knowing what’s deductible and following IRS rules is key. Also, you and your CPA need to know the difference between credits and deductions for businesses and how to claim them on your tax return.

In simple terms, a deduction is an amount you subtract from your income when you file so you don’t pay tax on it. A credit is an amount you subtract from the tax you owe. Here are credits you can claim when you file your taxes this year.

As for business deductions, claiming as many of them as you're entitled to can make a big difference for your bottom line.

So, the question now becomes …

What Deductions Can Your Small Business Claim?

When totaling up your business expenses, remember these common deductions:

Auto Expenses

If you use a car for business, you can deduct costs like gas, maintenance, and even depreciation. There are two ways to calculate this:

Actual Expense Method: Track and deduct all business-related car expenses, including depreciation.

Standard Mileage Rate: Deduct a set amount for every mile driven (67 cents per mile for 2024) plus business-related tolls and parking fees.

Startup Costs

Getting your business off the ground? You can deduct up to $5,000 in startup expenses the first year. The rest must be spread out over 15 years.

Legal and Professional Fees

Fees for lawyers, tax pros, or consultants are deductible. If the service benefits future years, spread the deduction across the life of the benefit.

Insurance

You can deduct premiums for business-related insurance, including:

Employee health insurance

Liability insurance

Property insurance (fire, theft, flood)

Business interruption insurance

Travel

Business trips? Deduct airfare, car expenses, lodging, meals, and even laundry. If you mix business with pleasure, only the business-related costs are deductible.

Interest

If you borrow for your business, the interest is tax-deductible. But if your profits exceed $25 million, only 30% of interest expenses are deductible under current laws.

Taxes

Yep, what you paid in taxes can reduce your tax burden. Certain taxes are deductible, like:

Sales tax on business supplies

Property taxes on business locations

Employer-paid payroll taxes

However, federal income taxes on business profits are not deductible.

Education

Training and education expenses that improve your current business skills are deductible. Just make sure it’s related to your existing work—not a new career.

Advertising and Promotion

Deduct the cost of promoting your business, such as business cards, websites, or even sponsoring local events—if there's a clear link to your business.

20% Pass-Through Deduction

If you run a pass-through business (like a sole proprietorship, partnership, or LLC), you may qualify to deduct up to 20% of your net income. This deduction lasts through 2025.

Employee Expenses

Employee salaries, payroll taxes, and benefits like health insurance are fully deductible.

Independent Contractors

The cost of hiring independent contractors, such as bookkeepers or cleaners, is deductible too.

Home Office

If you work from home, you can deduct a portion of your home expenses, like rent, utilities, and maintenance. The space must be used exclusively for business.

Don’t Miss These Additional Write-Offs

Here are some easy-to-overlook deductions:

Bank fees

Business association dues

Office supplies

Parking fees

Business gifts (up to $25 per gift)

Trade shows and seminars

Maximizing deductions takes careful planning, but it’s worth it. When in doubt, consult a tax professional to ensure you’re getting every tax break your business deserves.

Advanced Deductions

When it comes to working with a tax professional this year, Don’t leave money on the table by working with someone who doesn’t understand advanced strategies for reducing your tax burden.

Many CPAs don’t understand that it's possible to save outside the standard deductions. What are we talking about?

The IRS also provides tax incentives for business investments in fixed assets through Section 179 and Bonus Depreciation deductions. Let’s take a closer look at these.

These two deductions are often applied for manufacturing and real estate companies, but they can be creatively applied to many other businesses as well.

Bonus depreciation requires applying the deduction across all assets within a particular asset class, whereas Section 179 allows for more selective application on an asset-by-asset basis.

Both deductions must be taken in the tax year when the asset is placed into service. However, Section 179 allows flexibility to defer part of the expense, while bonus depreciation requires a set percentage to be applied.

Understanding the differences between these deductions helps optimize tax benefits. Let’s take a look.

Section 179

Section 179 gets its name from section 179 of the Internal Revenue Code. It allows business owners to write off the full cost of eligible property in the year it is purchased and put into use instead of deducting the depreciation over time.

Note: You cannot take a 179 deduction on property purchased in a previous year, even if this is the first year you used the property for business purposes.

Section 179 Eligibility

Property eligible for the Section 179 deduction is usually tangible personal property (usually equipment or office furniture) purchased for use in your business. If you use property for both personal and business purposes, you can only use a Section 179 deduction if the asset is used at least 51 percent of the time for business.

Section 179 Deduction Limitations

The total amount of purchases you can write off changes every time Congress updates IRC section 179 of the tax code. For tax years beginning in 2024, the maximum section 179 expense deduction is $1,220,000.

Section 179 + S Corp

Using a Section 179 tax deduction with your S Corp means you can deduct the full purchase amount of business equipment from your personal taxable income. Since an S Corp is a pass-through entity, when a Section 179 deduction is personally allocated to you from an S Corp or partnership, the income and expense are “passed through” to you, and you claim it on your individual tax return.

This means any income you earn from your S Corporation will be reduced by your Section 179 deductions, and you’ll only have to pay taxes on the reduced amount.

Bonus Depreciation

If you can't write off an asset immediately, you have to depreciate it. You deduct a percentage of the value each year until you've written off the entire cost.

It's also possible that you can take off extra for expenses that exceed the Section 179 limit, the first year as "bonus depreciation."

Starting in 2024, bonus depreciation rates decreased to 60 percent.

Bonus Depreciation Eligibility

Eligible assets extend to farm buildings and land improvements with a useful life of 1-20 years, including certain real estate improvements.

Bonus Depreciation Deduction Limitations

Unlike Section 179, there’s no business income limit, so it's usable even when reporting a business loss.

Combining Section 179 and Bonus Depreciation

You can use both Section 179 and bonus depreciation, especially when near the Section 179 deduction limits. However, state regulations may differ from federal rules, so be mindful of potential complications when filing state tax returns.

By strategically using Section 179 and bonus depreciation, business owners can effectively manage their tax liabilities while maximizing deductions on qualifying assets.

Income and Expense Evaluation: Use Section 179 if you have enough business income; otherwise, bonus depreciation is more suitable.

Consider Fixed Asset Purchases: If total fixed asset additions exceed Section 179 limits, bonus depreciation may be the better choice.

Tax Bracket Planning: Analyze current and future tax brackets to decide between accelerated or straight-line depreciation.