The Fractional Family Office: Your Financial ‘Dream Team’

Like life itself, the most important thing in financial management is who you trust enough to accompany you on your journey.

That’s why a great team makes all the difference. But finding the right people can seem like an impossible task.

Who can help you save money with advanced tax strategies?

Who can help you grow your money with elite investments?

Who can help you keep your money safe using the legal structures it takes to protect everything you’ve worked for?

And even if you’re fortunate enough to find these unicorns, how do you know if they have your best interests at heart?

Billionaires do this by hiring a "Family Office,” a staff dedicated to building and protecting their wealth. They have attorneys, CPAs, coaches and a host of other specialized services watching their back at every turn.

Now here’s the good news: In 2025, the Family Office concept is available to those of us who aren’t billionaires. This means you can have vetted professionals on staff and a network of providers vetted to handle all of your tax and investing needs no matter who you are, where you're located, or what investing you're doing.

Let’s take a closer look.

Start With Your Executive Team

You need proactive guidance to achieve your financial goals. Chances are you’ve worked with financial advisors and accountants before, but the likelihood of them being truly proactive in their approach is low.

In cases like these, you are the one doing the research, looking into tax strategies, reading articles about estate planning ….

A good fractional Family Office will take this work off your shoulders.

You’ll start by putting a strategic level Certified Public Accountant (CPA) on your team, someone who has the skills to take your tax burden as low as 0-10%. This partnership will be key for your wealth plan to be successful. The right CPA is someone who can implement the right tax strategies for you and give you proactive advice about saving money by improving your tax strategy.

Next, you’re going to grow your money with elite investments. This means hiring a Chief Financial Officer (CFO) and plugging into a deal network. To achieve a target 20-30% ROI, first you're going to hire the CFO to help you model investments.

You also need access to a deal network of high performing investments. The CFO is going to talk to you about blended ROI. This isn't just normal ROI like your financial advisor would talk to you about. And it's not just tax savings like a regular CPA would talk to you about. This is both of those combined.

The CFO is also going to guide you on how to protect your income through tax shelters or tax advantaged investments.

Finally, your executive team will be rounded out with a chief legal officer, basically an asset protection attorney. This will help you keep your money through legal structures that protect your wealth. This person will identify all the risk factors that you might be exposed to and help you mitigate them. They do this by creating the right entity structure and by providing ongoing estate planning and maintenance.

A Fractional Family Office Can Keep You Compliant

It's important that you get the right structure in place before you make investments in non-traditional assets. For example, Royal Legal Solutions helps investors use an LLC that is 100% owned by your IRA to incorporate cryptocurrency into their retirement accounts. This gives your crypto investments you the same tax-advantaged status as the IRA.

If you don't have a LLC (limited liability company) and a Self-Directed IRA structure set up already, your Family Office team can help.

They will also review your investment options and business structures to ensure they are up-to-date, compliant, and bulletproof against whatever the future holds. The right team will help you to ensure ongoing compliance with your state and local laws and tax requirements.

Your ‘Dream Team’ should give you actionable steps to take, making sure your asset protection plans are up-to-date and your financial dreams are closer to becoming a reality.

Private Foundations: A Practical Guide To Tax Savings

Private foundations enjoy tax-exempt status, but they are still subject to unique and sometimes complex tax rules under the Internal Revenue Code (IRC). From filing requirements to avoiding costly penalties, here's a streamlined overview of what private foundations need to know.

Understanding Governance and Deductions

Private foundations are governed by strict rules not applicable to public charities. In addition to normal “fiduciary” duties, they face penalties, often in the form of taxes in these areas:

Self-dealing: Prohibited transactions between the foundation and “disqualified persons” such as major donors or trustees.

Excess business holdings: Foundations cannot own too much of a business enterprise.

Jeopardy investments: Investments that risk the foundation’s ability to carry out its mission.

Taxable expenditures: Payments not aligned with charitable purposes, such as political lobbying or unapproved grants.

Net investment income: A 1.39% tax on income such as dividends, interest, and capital gains.

Contributions to private foundations are tax-deductible but may be subject to limits (typically 30% of adjusted gross income for individuals).

Identifying Unrelated Business Income (UBI)

UBI arises when a foundation earns income from a trade or business that is regularly carried on and not substantially related to its exempt purpose. Passive income (e.g., dividends, royalties) is generally excluded—unless it’s debt-financed.

If UBI exceeds $1,000, the foundation must file Form 990-T. Tax is assessed at standard corporate rates, and estimated taxes may be required if expected liability exceeds $500.

Careful tracking of expenses related to UBI is critical for reducing tax liability. Expenses must be directly tied to the unrelated business and reasonably allocated.

Calculating the Net Investment Income Tax

Private foundations are subject to a 1.39% tax on net investment income. This includes:

Interest (except tax-exempt)

Dividends

Rents and royalties

Capital gains

Income from limited partnerships

Deductions may include necessary expenses incurred to generate or manage investment income. However, previously paid excise taxes cannot be deducted.

Meeting the Annual Distribution Requirement

Nonoperating foundations must distribute at least 5% of their average annual noncharitable-use assets. Qualifying distributions include grants to 501(c)(3) public charities and certain administrative expenses.

Failure to meet the minimum distribution requirement results in a 30% excise tax on undistributed income, with a 100% tax imposed on persistent shortfalls.

Maintaining Expenditure Responsibility

When making grants, especially to foreign or nonqualified organizations, a private foundation must follow IRS expenditure responsibility rules. This includes:

Conducting a pre-grant inquiry.

Establishing a written grant agreement.

Requiring periodic reports from the grantee.

Reporting to the IRS annually via Form 990-PF.

Investigating any misuse of funds.

Failure to comply may result in excise taxes and jeopardize the foundation’s tax-exempt status.

Recognizing Operating Foundations

Unlike nonoperating foundations, operating foundations directly conduct charitable activities. While they share many tax rules with nonoperating foundations, key distinctions include:

Donations qualify for higher charitable deduction limits (up to 60% of AGI).

They are exempt from annual distribution excise taxes.

They must meet both an income test and one of three operational tests (assets, endowment, or support) in three out of four years.

Operating foundations are less common and typically more complex to manage.

Avoiding Self-Dealing Pitfalls

Self-dealing rules prevent transactions between the foundation and disqualified persons. Common violations include:

Paying personal travel expenses.

Renting property from a family member.

Awarding scholarships to relatives.

Penalties include a 10% excise tax on the self-dealer and a 5% tax on any foundation manager who knowingly participated. If not corrected, second-tier penalties of up to 200% may apply.

Applying for Tax-Exempt Status and Filing Requirements

To qualify for exemption under IRC Section 501(c)(3), an organization must legally form as a nonprofit corporation or trust and include clauses in its governing documents that support a charitable purpose.

Once established, the foundation must apply to the IRS using Form 1023 or the simplified 1023-EZ. If the application is submitted within 27 months of formation, the organization will be treated as exempt retroactively from its formation date.

Annually, all private foundations—regardless of income or activity—must file IRS Form 990-PF. Failure to file on time can result in daily penalties.

Final Thoughts

Private foundations play a vital role in philanthropy but must navigate a landscape of regulatory requirements and potential tax pitfalls. Understanding these obligations—from filing and reporting to expenditure rules and excise taxes—is essential to maintaining tax-exempt status and fulfilling charitable missions effectively.

Can My Husband and I Own Our Business Together as a Sole Proprietorship?

There are some cases where a couple who run a business together wouldn’t be interested in creating a formal business entity.

The question then becomes: can that business, being run by a married couple, be considered a sole proprietorship?

The answer is yes. The IRS allows a lone exemption for married couples who want to structure their business as a sole proprietorship.

Before going into details on that, there are typically four different kinds of business structures that the IRS recognizes. Those include:

Sole proprietorships

Partnerships

Limited Liability Companies

Corporations

In order for the business you run with your spouse to qualify as a sole proprietorship, the following conditions must be met:

There must be no other employees actively engaged with the business. This includes children or other relatives.

Both spouses must materially participate in the running the business.

With those requirements met, each spouse would be required to file their own Schedule C, reporting their individual share (usually an even split) of the business’s income. Each spouse in the husband-and-wife business (sole proprietor or partnership or other) would also need to file a separate self-employment tax form.

Should My Spouse and I Run Our Business as a Sole Proprietorship?

This, of course, is a separate issue entirely. The big advantage of a sole proprietorship is that it’s one of the easiest business structures to establish. The major disadvantage of this structure is that you and your spouse are 100% liable if the business fails. Sole proprietorships offer no protection from creditors.

Another option that many married couples employ is a partnership. For tax purposes, it can be easier to file since there is only one form involved. On the other hand, the business will be required to obtain a tax identification number. Partnerships might also be subject to state and federal regulations. The major upside, however, is that partnerships offer more opportunities for growth.

There are no regulations that state that if you start a business as a joint venture LLC, which for tax purposes is considered a sole proprietorship, you cannot later change the structure of the business to a partnership, LLC, or anything else. For many married couples, having the option to start as a sole proprietorship affords them the opportunity to hit the ground running. It’s a simple and effective means of getting their business started without needing to file numerous petitions with state and federal agencies.

What makes sense for your business in the early days, however, may not make sense down the road.

3 Key Tax Benefits of Using an LLC Structure

Limited Liability Companies have many useful properties for investors. Most of my clients approach me about forming Traditional LLCs or Series LLCs for asset protection, but often are completely unaware of the potential tax benefits their entity may provide.

Today, let’s talk a bit about the tactics you can use to minimizing your tax liabilities. Specifically, we will be taking a closer look at the tax benefits of an LLC structure.

Tax Status Flexibility

One of the appealing tax benefits of LLCs is that you get to choose the manner in which it is taxed. But owners of Series LLCs don’t have to miss out on the fun. In fact, if you own a Series LLC, you can tax each Series differently if you desire. What exactly does that mean? Let’s take a closer look at how LLCs are taxed.

You may make your pick from any of the following three tax status elections when forming an LLC (or Series within a Series LLC):

Disregarded Entity. A pass-through entity, also commonly referred to as a flow-through entity allows taxes to be passed onto your personal tax return. Learn much more about the benefits of pass-through tax treatment for real estate investors from our previous article on the subject. Single-member LLCs and married couple LLCs are typically treated this way automatically in most jurisdictions.

Partnership. Partnership taxation is the default status of multi-member LLCs, but they may choose to change to S-Corporation or Disregarded Entity status. In entities taxed as partnerships, each member receives a Schedule K-1 and reports their share of the profits and losses. This information, along with a completed Form 1065 for partnership taxation, will be attached to members’ tax returns. In this way, the company isn’t billed, but the members each pay their fair share of the taxes.

S-Corporation. This status makes sense for anyone who would benefit from the lower tax rate on the entity’s first $75,000 in income. It’s treated more like a corporation, albeit with different provisions than the more complex C-Corporation. It also comes with a super sexy form called Form 8332. Filling it out might not be a blast, but the savings sure can be for certain investors.

Note that there is an exception to the flexibility norm. Single-member LLCs are more limited and may be forced to file as a sole proprietorship, then report income or losses on their personal returns. It is also important to be aware that the above are simply tax classifications rather than different types of entities. It can be easy to get the impression that an S-Corporation is an entity when indeed it is a tax status, as a C-Corporation is an entity.

Which tax option will be best for you? As with most answers in the financial realm, you’ll find that it depends on your individual circumstances, status, and ambitions in the real estate business. Only a qualified attorney and CPA should be trusted to give tax advice.

Deductions and Credits Galore For Those Willing to Look

If you’re serious about lowering your tax bill you know the power of deductions. So we recommend that you deduct, deduct, deduct everything that you can. No business expense is too small or inexpensive. See if you qualify for fuel deductions, and take a good written record of everything you really need for work and its cost. It may seem silly if you’re looking at many small receipts or expenses, but the old adage about how they tend to add up is true.

The fact that you may not be aware of deduction and credit opportunities is yet another good reason to have a solid CPA and attorney on your real estate dream team. These pros will often point out savings options you didn’t even know you were missing out on. So go forth and deduct shamelessly. It’s a win-win for both client and CPA.

Personal Assets May Be Leased to the LLC

If a valuable assets drag you into a higher tax bracket, an LLC offers a handysolution. You may be able to minimize this situation by leasing the asset to yourself (specifically, your LLC) with a formal leasing agreement. Such arrangements lower taxable income and often allow for deductions.

For example, a home office is an item you lean on come Tax Season when you’re deduction hunting. Learn more details about the home office deduction and who can qualify from our previous educational resource on the subject. Home offices may not only be deducted from your taxes, but also leased back to your LLC. When that leasing agreement goes through, you can write it off and claim it as a business expense. The fact that this type of business expense

Optimize Your LLC Tax Strategy With The Pros at Royal Legal Solutions

Between the asset protection and tax benefits, LLCs may begin to seem like a no-brainer. But to get the right entity that will do the best possible job for you, you may need Our crack team of attorneys and the CPAs we work with can assist you through any tax concerns you may have. As investors ourselves, we may have some more tips that you haven’t yet learned to exploit. Which ones will apply to you will depend on your personal circumstances.

If you are wondering how Royal Legal Solutions can help you save on your taxes, our consultants are happy to explain your options to you, answer your questions, and when you’re ready, set up your personalized consultation. We look forward to helping you keep more of your income where it belongs: in your bank account.

Find out about the tax savings strategies that you can implement as a real estate investor or entrepreneur by taking our Tax Discovery quiz. We'll use this information to prepare to have a productive conversation. At the end of the quiz, you'll have an opportunity to schedule your consultation. TAKE THE TAX DISCOVERY QUIZ

Short-Term Rental Cost Segregation Study Helps With 2025 Taxes

Rental Property Depreciation is a killer strategy for reducing taxes.

And short-term-rental (STR) owners need a cost segregation study to reclassify parts of their property from a standard 39-year life to shorter lifespans (say, 5 or 15 years.)

Even as bonus depreciation phases out to 0 percent by 2027, a cost segregation study can still maximize your property’s depreciation benefits.

Let’s take a closer look.

How to Use Rental Property Depreciation to Your Advantage

Rental property depreciation can be a game-changer when it comes to reducing taxes for your short-term rental (STR) business. And if you’re looking to deepen your role in the real estate industry beyond investing, learning how to become a real estate agent can open new professional opportunities while complementing your investment strategies.

By leveraging strategies like accelerated depreciation, you can take larger deductions in the early years of owning a property, freeing up cash flow and lowering your tax bill. Here’s how it works and why it’s worth considering.

What Is Accelerated Depreciation?

Accelerated depreciation allows assets to lose value more quickly in the earlier years of ownership, rather than spreading the deductions evenly over the property’s lifespan.

Why does this matter?

Bigger tax savings earlier on: You can claim larger deductions in the first few years the property is in service.

Lower taxable income: Reducing your reported profit means you may qualify for a lower tax bracket.

Improved cash flow: With a lower tax bill, you can reinvest savings into your business or other opportunities.

How Does A Cost Segregation Study Fit In?

The IRS typically allows residential rental properties to depreciate over 27.5 years and commercial properties over 39 years. However, not every part of a property needs to follow this timeline.

Look at it this way. When you buy or construct a property, it includes more than just the building itself. Think about:

Plumbing fixtures

Carpeting

Sidewalks

Fencing

If purchased separately, these items could be depreciated over 5, 7, or 15 years. A cost segregation study helps identify these shorter-life assets and accelerates their depreciation, giving you more tax savings upfront.

How Does a Cost Segregation Study Work?

A cost segregation study breaks down the purchase price or construction cost of your property into categories with different depreciation schedules. Here’s the process:

Identify short-life components: Examples include electrical outlets for appliances (5 years) or landscaping improvements (15 years).

Reallocate costs: On average, 20-40% of a property’s components can qualify for accelerated depreciation.

Calculate tax savings: By writing off these assets sooner, you significantly reduce your taxable income in the early years.

What’s Involved in a Cost Segregation Study?

A high-quality cost segregation study includes:

Review of property records: Cost details, blueprints, and other documentation.

On-site inspection: To identify and assess qualifying components.

Comprehensive reporting: Detailed findings with a breakdown of depreciation categories. If records are incomplete, professionals can still estimate values based on the property inspection.

When Should You Conduct a Cost Segregation Study?

Timing matters!

Best time: The year a property is purchased, remodeled, or constructed.

Planning ahead: If you’re building or renovating, consider a study before finalizing the infrastructure. For STR investors, acting early ensures you maximize your deductions as soon as the property is in service.

How Much Can You Save?

Let’s crunch the numbers with an example:

Imagine you own a short-term rental valued at $800,000.

Without cost segregation:

Depreciate over 39 years: $20,512 per year

Tax savings (at 37% rate): About $4,600/year

With cost segregation:

$100,000 of electrical fixtures (5 years)

$100,000 of plumbing fixtures (7 years)

$100,000 for parking, landscaping and storm sewers (15 years)

Now, instead of a flat $800,000 depreciating over 39 years, you allocate $300,000 for accelerated depreciation. This leads to significantly larger tax savings in the first year and beyond.

DIY Cost Segregation Studies—Are They Worth It?

While you can identify some short-life assets on your own, working with a tax professional ensures you get the full benefit of a cost segregation study.

There are two main approaches:

“Rule of thumb” method: Estimates based on similar properties; less reliable and higher risk.

Engineering approach: A detailed review using actual cost records; more accurate and preferred by the IRS. A professional specializing in cost segregation will typically use the engineering approach, reducing your audit risk and maximizing your tax savings.

Bonus Depreciation is Phasing Out: Act Now to Maximize Savings

Rental property depreciation, especially when paired with a cost segregation study, is a powerful tool for STR investors. By accelerating depreciation on certain components, you can:

Free up cash flow

Lower your taxable income

Reap significant tax savings in the early years of ownership

As the saying goes, all good things must come to an end. Under current law, bonus depreciation is being phased out:

2024: Reduced to 60%

2025: Drops to 40%

2026: Down to 20%

2027 and beyond: Completely eliminated (0%)

If you’re an investor looking to take advantage of this tax-saving strategy, now is the time. The sooner you act, the greater your potential savings before bonus depreciation disappears entirely.

Want to unlock these benefits? Reach out to a tax professional to see if a cost segregation study is right for your property. The savings could be substantial, so don’t miss this window of opportunity to optimize your cash flow and reduce your tax burden!

BONUS: 12 Common Questions About Cost Segregation Studies

1. What Is a Cost Segregation Study?

Every property is made up of a variety of assets, and each one has a different expected useful life. For instance, tile flooring is much more durable than carpet, right?

Tax law accounts for these differences and guides how capital expenditures should be depreciated. Using the Modified Asset Cost Recovery System (MACRS):

Residential real property is typically depreciated over 27.5 years.

Nonresidential real property is depreciated over 39 years.

Without a cost segregation study, all assets in a property would default to these timelines, even though it doesn’t make sense for shorter-lived components like carpet. Cost segregation adjusts this, giving you more accurate depreciation timelines—and better tax savings.

2. How Are Building Assets Categorized for Depreciation?

A cost segregation study breaks down a property into individual components, assigns costs to each using IRS-approved pricing guides, and places them into different categories based on their depreciation timelines. Here are some common categories:

15-Year Assets: Land improvements like parking lots, landscaping, drainage systems, outdoor pools, and sidewalks. By moving these assets into shorter-lived categories, they depreciate faster, which means more tax savings upfront and better cash flow.

3. Is Cost Segregation Worth It For Rental Property Investors?

Yes, cost segregation can offer a significant return on investment! While the cost of the study depends on the size and complexity of the property, the benefits often far outweigh the expense. Beyond accelerated depreciation, cost segregation can:

Provide data for future tax strategies.

Be updated if new tax laws or opportunities arise. To get a clearer picture of potential savings, many providers offer free estimates after reviewing your property details.

4. What Types of Real Estate Qualify for Cost Segregation?

Cost segregation isn’t just for office buildings or hotels—it can be applied to nearly all types of commercial and residential real estate, including short-term rentals. Popular property types include:

Garden-style apartment complexes

Manufacturing facilities

Auto dealerships

Self-storage facilities

5. Does Cost Segregation Create New Deductions?

No, cost segregation doesn’t create new deductions. Instead, it accelerates existing deductions by shifting them to earlier years of ownership. This lets you take advantage of the time value of money by getting tax savings sooner.

6. Can I Do a Cost Segregation Study Myself?

While cost segregation may seem straightforward, a quality study requires expertise. A professional will conduct a detailed forensic analysis of the property, breaking out assets, assigning costs, and ensuring compliance with IRS rules. This level of precision is key to maximizing your tax savings and minimizing audit risks.

7. When Is the Best Time to Perform a Cost Segregation Study?

The best time to perform a cost segregation study is right after a property is purchased or constructed. This ensures the study accurately reflects the assets in place when the property is first put into service, maximizing your tax benefits from day one.

8. How Far Back Can You Do a Cost Segregation Study?

You can conduct a “look-back” cost segregation study for properties purchased in previous years. This allows you to claim missed depreciation without amending past tax returns by filing Form 3115 to catch up on deductions.

9. Can Cost Segregation Studies Be Used as a Planning Tool?

Absolutely! Cost segregation can be integrated into your tax planning strategy before a property is purchased or constructed. For example, you can:

Design buildouts to maximize assets eligible for accelerated depreciation.

Incorporate energy-efficient features to qualify for additional credits like IRC Sec. 179D or Sec. 45L.

Align depreciation deductions with cash flow needs. The data from a cost segregation study can also set you up for future tax benefits, such as partial asset dispositions or tracking capital improvements.

10. How Does Bonus Depreciation Relate to Cost Segregation?

Bonus depreciation allows you to take an additional write-off for assets with a class life of less than 20 years. It’s a powerful tool that complements cost segregation, as the study identifies assets eligible for bonus depreciation. Under the Tax Cuts and Jobs Act, the bonus depreciation rate was 100% for assets placed in service between 2017 and 2022. This rate dropped to 80% in 2023 and will phase out entirely by 2027. Despite the reduction, cost segregation still provides significant tax benefits.

11. Is Cost Segregation Useful for Renovation Projects?

Yes! While cost segregation is commonly used for newly purchased or constructed properties, it’s also valuable for properties undergoing major renovations. By quantifying and categorizing assets before they’re retired, you can take advantage of the partial asset disposition (PAD) election to write off the remaining value of disposed assets. Renovated assets classified as Qualified Improvement Property (QIP) may also qualify for accelerated depreciation or bonus depreciation.

12. What Is Qualified Improvement Property (QIP) and How Is It Connected to Cost Segregation?

QIP refers to interior improvements made to nonresidential buildings after they’ve been placed in service, excluding structural changes, expansions, or upgrades like elevators. Thanks to the CARES Act, QIP now has a 15-year recovery period, making it eligible for bonus depreciation. Cost segregation helps identify and categorize QIP assets, ensuring they are accurately valued for depreciation purposes. This is especially beneficial for landlords providing tenant buildout allowances, allowing for faster tax savings on these investments.

Deductions for 2025 (Tax Year 2024): A Beginner's Guide

You’ve worked hard to get where you are, and one thing you’ve no doubt learned along the way is that tax season is usually the biggest pain when you’re managing your accounts.

And if you’re not familiar with the deductions you may qualify for that pain is even worse.

Don’t pull your hair out over the confusing (and ever-changing) tax code— just need some help from the right advisors. Then you can lower your overall tax bill and keep more of your hard-earned money.

In this guide, we’ll break down the essentials of tax deductions for tax year 2024 (what you’ll file in 2025). Whether you’re an individual filer, a small business owner, or someone looking to maximize advanced tax-saving strategies, this article will provide you with the tools you need to take control of your taxes.

We’ll start with standard deductions, the simplest way to lower your taxable income. Then, we’ll explore business deductions, which can help entrepreneurs and freelancers save big. Finally, we’ll dive into advanced deductions, perfect for those looking to optimize their finances with more complex tax strategies.

Let’s get started on your path to smarter tax filing in 2025!

Standard Deductions

As usual, taxpayers, including business owners, can choose between standard deductions and itemized deductions when filing their 2024 income taxes.

(The standard deduction or itemized deductions differ from self-employed business expense deductions. To maximize your deductions across all income types, we highly recommend you get the tax advice you need for your specific situation.)

Many prefer the standard deduction offered by the IRS due to its simplicity. This fixed amount reduces taxable income and varies based on your filing status. The IRS has increased the standard deduction to account for annual inflation. The standard deduction for married couples filing jointly for tax year 2024 rose to $29,200, an increase of $1,500 from tax year 2023.

For single taxpayers and married individuals filing separately, the standard deduction rises to $14,600, an increase of $750 from 2023. For heads of households, the standard deduction is $21,900, an increase of $1,100.

The standard deduction amounts for tax year 2024 (taxes filed in 2025) and for tax year 2025 (taxes filed in 2026) are as follows:

Filing status

2024 standard deduction

2025 standard deduction

Single

$14,600

$15,000

Head of household

$21,900

$22,500

Married filing jointly

$29,200

$30,000

Married filing separately

$14,600

$15,000

Business Deductions

The more tax deductions your business claims, the lower your taxable profit—and that means more money in your pocket.

But knowing what’s deductible and following IRS rules is key. Also, you and your CPA need to know the difference between credits and deductions for businesses and how to claim them on your tax return.

In simple terms, a deduction is an amount you subtract from your income when you file so you don’t pay tax on it. A credit is an amount you subtract from the tax you owe. Here are credits you can claim when you file your taxes this year.

As for business deductions, claiming as many of them as you're entitled to can make a big difference for your bottom line.

So, the question now becomes …

What Deductions Can Your Small Business Claim?

When totaling up your business expenses, remember these common deductions:

Auto Expenses

If you use a car for business, you can deduct costs like gas, maintenance, and even depreciation. There are two ways to calculate this:

Actual Expense Method: Track and deduct all business-related car expenses, including depreciation.

Standard Mileage Rate: Deduct a set amount for every mile driven (67 cents per mile for 2024) plus business-related tolls and parking fees.

Startup Costs

Getting your business off the ground? You can deduct up to $5,000 in startup expenses the first year. The rest must be spread out over 15 years.

Legal and Professional Fees

Fees for lawyers, tax pros, or consultants are deductible. If the service benefits future years, spread the deduction across the life of the benefit.

Insurance

You can deduct premiums for business-related insurance, including:

Employee health insurance

Liability insurance

Property insurance (fire, theft, flood)

Business interruption insurance

Travel

Business trips? Deduct airfare, car expenses, lodging, meals, and even laundry. If you mix business with pleasure, only the business-related costs are deductible.

Interest

If you borrow for your business, the interest is tax-deductible. But if your profits exceed $25 million, only 30% of interest expenses are deductible under current laws.

Taxes

Yep, what you paid in taxes can reduce your tax burden. Certain taxes are deductible, like:

Sales tax on business supplies

Property taxes on business locations

Employer-paid payroll taxes

However, federal income taxes on business profits are not deductible.

Education

Training and education expenses that improve your current business skills are deductible. Just make sure it’s related to your existing work—not a new career.

Advertising and Promotion

Deduct the cost of promoting your business, such as business cards, websites, or even sponsoring local events—if there's a clear link to your business.

20% Pass-Through Deduction

If you run a pass-through business (like a sole proprietorship, partnership, or LLC), you may qualify to deduct up to 20% of your net income. This deduction lasts through 2025.

Employee Expenses

Employee salaries, payroll taxes, and benefits like health insurance are fully deductible.

Independent Contractors

The cost of hiring independent contractors, such as bookkeepers or cleaners, is deductible too.

Home Office

If you work from home, you can deduct a portion of your home expenses, like rent, utilities, and maintenance. The space must be used exclusively for business.

Don’t Miss These Additional Write-Offs

Here are some easy-to-overlook deductions:

Bank fees

Business association dues

Office supplies

Parking fees

Business gifts (up to $25 per gift)

Trade shows and seminars

Maximizing deductions takes careful planning, but it’s worth it. When in doubt, consult a tax professional to ensure you’re getting every tax break your business deserves.

Advanced Deductions

When it comes to working with a tax professional this year, Don’t leave money on the table by working with someone who doesn’t understand advanced strategies for reducing your tax burden.

Many CPAs don’t understand that it's possible to save outside the standard deductions. What are we talking about?

The IRS also provides tax incentives for business investments in fixed assets through Section 179 and Bonus Depreciation deductions. Let’s take a closer look at these.

These two deductions are often applied for manufacturing and real estate companies, but they can be creatively applied to many other businesses as well.

Bonus depreciation requires applying the deduction across all assets within a particular asset class, whereas Section 179 allows for more selective application on an asset-by-asset basis.

Both deductions must be taken in the tax year when the asset is placed into service. However, Section 179 allows flexibility to defer part of the expense, while bonus depreciation requires a set percentage to be applied.

Understanding the differences between these deductions helps optimize tax benefits. Let’s take a look.

Section 179

Section 179 gets its name from section 179 of the Internal Revenue Code. It allows business owners to write off the full cost of eligible property in the year it is purchased and put into use instead of deducting the depreciation over time.

Note: You cannot take a 179 deduction on property purchased in a previous year, even if this is the first year you used the property for business purposes.

Section 179 Eligibility

Property eligible for the Section 179 deduction is usually tangible personal property (usually equipment or office furniture) purchased for use in your business. If you use property for both personal and business purposes, you can only use a Section 179 deduction if the asset is used at least 51 percent of the time for business.

Section 179 Deduction Limitations

The total amount of purchases you can write off changes every time Congress updates IRC section 179 of the tax code. For tax years beginning in 2024, the maximum section 179 expense deduction is $1,220,000.

Section 179 + S Corp

Using a Section 179 tax deduction with your S Corp means you can deduct the full purchase amount of business equipment from your personal taxable income. Since an S Corp is a pass-through entity, when a Section 179 deduction is personally allocated to you from an S Corp or partnership, the income and expense are “passed through” to you, and you claim it on your individual tax return.

This means any income you earn from your S Corporation will be reduced by your Section 179 deductions, and you’ll only have to pay taxes on the reduced amount.

Bonus Depreciation

If you can't write off an asset immediately, you have to depreciate it. You deduct a percentage of the value each year until you've written off the entire cost.

It's also possible that you can take off extra for expenses that exceed the Section 179 limit, the first year as "bonus depreciation."

Starting in 2024, bonus depreciation rates decreased to 60 percent.

Bonus Depreciation Eligibility

Eligible assets extend to farm buildings and land improvements with a useful life of 1-20 years, including certain real estate improvements.

Bonus Depreciation Deduction Limitations

Unlike Section 179, there’s no business income limit, so it's usable even when reporting a business loss.

Combining Section 179 and Bonus Depreciation

You can use both Section 179 and bonus depreciation, especially when near the Section 179 deduction limits. However, state regulations may differ from federal rules, so be mindful of potential complications when filing state tax returns.

By strategically using Section 179 and bonus depreciation, business owners can effectively manage their tax liabilities while maximizing deductions on qualifying assets.

Income and Expense Evaluation: Use Section 179 if you have enough business income; otherwise, bonus depreciation is more suitable.

Consider Fixed Asset Purchases: If total fixed asset additions exceed Section 179 limits, bonus depreciation may be the better choice.

Tax Bracket Planning: Analyze current and future tax brackets to decide between accelerated or straight-line depreciation.

What’s New for Advanced Deductions … According to the Internal Revenue Service

Section 179 deduction dollar limits. For tax years beginning in 2024, the maximum section 179 expense deduction is $1,220,000. This limit is reduced by the amount by which the cost of section 179 property placed in service during the tax year exceeds $3,050,000.Also, the maximum section 179 expense deduction for sport utility vehicles placed in service in tax years beginning in 2024 is $30,500.

Phase down of special depreciation allowance. The special depreciation allowance is 60% for certain qualified property acquired after September 27, 2017, and placed in service after December 31, 2023, and before January 1, 2025 (other than certain property with a long production period and certain aircraft). Property with a long production period and certain aircraft placed in service after December 31, 2023 and before January 1, 2025 is eligible for a special depreciation allowance of 80% of the depreciable basis of the property. The special depreciation allowance is also 60% for certain specified plants bearing fruits and nuts planted or grafted after December 31, 2023 and before January 1, 2025.

Remember: Staying informed about the latest tax changes is crucial to avoid costly mistakes. The choices you make for your business this year will directly impact your tax obligations next year.

The right tax professionals can help you navigate complex regulations, maximize tax benefits, and align with current tax laws.

Lower level CPAs may not even know it's possible to save outside the standard deductions, and even more competent CPAs tend to only know about S-Corporations and real estate investing.

What you want is a CPA who earns a high income, just like you, and who has found a way to pay nearly $0 in tax by leveraging advanced strategies. It's even better if they have an MBA and can perform Chief Financial Officer functions. When you work with a CPA at that level, you’ll find lots of ways to save on tax, even if you're a W2 employee (or active 1099) with zero investment experience.

In turn, that improves your cash flow and gives you more cash to reinvest in your business's success and in your long-term strategy for building generational wealth.

2025 IRS Code Updates: Opportunities for the 2024 Tax Year

Let's face it, paying taxes stinks.

No one likes to think about tax code updates, but the fact is the 2025 tax season is here, things have changed, and you can’t avoid it!

Failing to plan is planning to fail is a cliche, sure, but it’s the truth. If you don’t work with someone who is familiar with the tax code updates, you’ll leave money on the table now that tax season is rearing its ugly head again.

There were several tax code updates for the 2024 tax year that W2 (or active 1099) workers and business owners need to know about .

To help you navigate the murky waters of the 2025 tax season, we compiled a list of the four most important tax code updates from that session.

Work with your CPA who knows about advanced strategies. Someone with an MBA who can perform Chief Financial Officer functions. With their help and the information below, you’ll navigate complex tax decisions and make building your financial future seem easy.

#1 Tax Code Updates On Income Brackets

How much you pay in taxes depends on your income and your filing status ( whether you’re single, married, or filing jointly).

Your income isn’t taxed at a single, flat rate. Instead, it’s divided into tax brackets. You may pay several different tax rates on various parts of your earnings.

The 2024 tax brackets apply to income earned last year (what you’ll report on tax returns filed in 2025):

Tax rate

Single Taxable Income

Married Filing Jointly Taxable Income

Married Filing Separately Taxable Income

Head of Household Taxable Income

10%

Up to $11,600

Up to $23,200

Up to $11,600

Up to $16,550

12%

$11,601 to $47,150

$23,201 to $94,300

$11,601 to $47,150

$16,551 to $63,100

22%

$47,151 to $100,525

$94,301 to $201,050

$47,151 to $100,525

$63,101 to $100,500

24%

$100,526 to $191,950

$201,051 to $383,900

$100,526 to $191,950

$100,501 to $191,950

32%

$191,951 to $243,725

$383,901 to $487,450

$191,951 to $243,725

$191,951 to $243,700

35%

$243,726 to $609,350

$487,451 to $731,200

$243,726 to $365,600

$243,701 to $609,350

37%

$609,351 or more

$731,201 or more

$365,601 or more

$609,351 or more

#2 Standard Deductions Increase For Everyone

The standard deduction allows you to save money on taxes by reducing your taxable income. The standard deduction for married couples filing jointly for tax year 2024 increased to $29,200, $1,500 more than tax year 2023.

For single taxpayers and married individuals filing separately, the standard deduction is $14,600 for 2024, an increase of $750 from the previous year.

For heads of households, the standard deduction will be $21,900 for tax year 2024, an increase of $1,100.

You can also leverage standard deductions by paying your children to work for you (up to the standard deduction amount). Here are some general rules that you should follow if you have children who can work for you:

Children have to be doing work for you.

Pay your children in a way that is commensurate with their age and the tasks they are doing.

Although technically, you don't have to file a tax return for less than $12,950 in wages. It's probably a good idea to do so just so that you have proof that you paid your children in case you get audited.

#3 Safeguard Your Health And Money With HSA Contributions

You can reduce your taxable income by contributing to a health savings account. This account helps you pay for medical expenses.

The deductible contribution increased to $3,650 from $3,600 for a single person. For families, the HSA deductible went to $7,200 from $7,300.

Health Savings Accounts (HSAs) are a smart way to save money for medical expenses. Why? Because the money you put in—and use for qualified medical costs—is tax-free.

Before contributing to an HSA, you must meet these requirements:

You’re enrolled in an HSA-eligible health plan.

For 2024, this means:

A deductible of at least $1,600 (self-only) or $3,200 (family)

An out-of-pocket max no higher than $8,050 (self-only) or $16,100 (family)

You don’t have conflicting coverage.

This includes non-HSA-eligible health plans or a full-purpose health care Flexible Spending Account (FSA).

You’re not enrolled in Medicare.

You’re not claimed as a dependent on someone else’s tax return.

One more “catch”: You can’t contribute unlimited amounts. The IRS sets a cap on how much you can contribute to your HSA. This limit includes contributions made by both you and your employer.

For example, if your 2024 HSA limit is $4,150 and your employer adds $1,000, you can only contribute $3,150. However, if you’re 55 or older, you can also make an extra $1,000 catch-up contribution.

2024 HSA Contribution Limits

Self-only coverage: $4,150

Family coverage: $8,300

Catch-up contribution (age 55+): Add $1,000

Here’s what determines how much you can contribute:

Whether you have self-only or family health coverage

Your age (55 or older? You get that catch-up boost!)

#4 Tax Code Updates Means More Money For Your Family

The 2024 lifetime estate and gift tax exemption surged from $12.92 million to $13.61 million (double for married couples). This shields most people from having to pay federal gift tax.

But if you DO have to pay … For 2024, the annual gift tax limit is $18,000. ( up $1,000 from 2023 since the gift tax is one of many tax amounts adjusted annually for inflation.)

That means you can give your child $18,000 (or $36,000 for couples) to each child, grandchild, or person without filing taxes on the gift.

Key Takeaways

No one wants to think about paying taxes before taxes are due. But, you should plan to keep more money in your pocket and out of Uncle Sam's coffers.

To hold onto your nest, you must stay abreast of the tax code updates that may affect you in 2025.

Some critical updates that may affect you as a real estate investor include the changes to:

Tax brackets

Standard deductions

HSA contributions

Lifetime estate and gift tax exemption

Tax, Investing, and Legal Strategies for Medical Professionals

High-earning medical professionals eventually learn a hard lesson:

The more they earn, the more they pay in income taxes.

And since physicians and other medical professionals rank among some of the highest-paid individuals in the United States, they need tax planning and investment strategies that will protect their assets and build real generational wealth they can pass to their children and grandchildren.

Hard-working doctors and other healthcare pros can take advantage of all the tax deductions, tax credits and tax exemptions that Congress and the Internal Revenue Service (IRS) make possible to reduce their taxable income.

But there are also lesser-known strategies which, when leveraged correctly, can reduce your tax burden and deliver a sound financial plan that gives you what we call “time freedom.”

Here I’ll introduce some of the tax, investing and legal strategies our medical professional clients use.

Tax Strategies for Medical Professionals

As a busy healthcare professional, you work hard to provide quality care to your patients, juggle administrative work, and balance your work with life and demands at home.

That’s why working to optimize your tax situation is probably not at the top of your priorities.

Deep down, however, you know that tax planning should be a key component of your wealth management strategy.

If you are employed by a hospital, a private practice, or a government healthcare department, you’re probably a W2 worker. W2 employees are taxed on gross income first, meaning the IRS takes their cut before you receive your paycheck.

But if you’re a business owner or investor (with the correct structures in place), you can pay the IRS quarterly on your net income after expenses.

To put it another way, when investing through a properly structured entity, your investment income gets the same tax treatment as a business. This allows you to use your money before deducting taxes.

If you’re like most of our clients, you've been told there isn't much you can do to lower your taxes beyond taking deductions or using retirement vehicles like 401ks and IRAs.

This simply isn’t true.

That’s why finding the right CPA to work with is so crucial. You need someone who knows what they’re talking about. It's important to understand there are different tiers of CPAs:

Many CPAs don’t understand that it's possible to save outside the standard deductions. A high-level CPA is someone who earns a high income themselves, someone who has personally found a way to pay nearly $0 in tax by leveraging advanced strategies.

The right CPA helps our medical professional clients achieve and maintain tax rates in the 0-10% range. This accelerates your overall cash flow and net worth.

If you find a CPA with an MBA and who can perform Chief Financial Officer functions, even better— these folks will be able to help you navigate complex tax decisions and make it seem easy.

When you work with that level of CPA, you'll start to find creative (but completely legal) ways to save taxes, even if you're a medical professional with zero investment experience. And that savings can be invested in equally creative, equally overlooked ways.

Such as …

Investing Strategies For Medical Professionals

The median wage for medical professionals (everything from dental hygienists, physicians and surgeons, to registered nurses) was $80,820 in 2023—much higher than the median annual wage (for all occupations) of $48,060. (Source)

However, at a certain point these high-salary professionals realize they need to take steps to shelter their income from overtaxation. And while saving money on tax is important, but the real magic happens once our medical professionals start re-investing those tax savings into tax advantaged deals.

These include:

Private Foundations

A Private Foundation is a self-funded nonprofit organization that shelters income, allowing you to bypass traditional capital gains tax and take advantage of a much lower excise tax rate.

When using the Private Foundation for income sheltering and high-performance investments, the compounding effect can lead to much better returns than traditional investing.

The Private Foundation can even replace your W2 income with a director’s salary for managing the Foundation.

Depreciation Deals

Bonus depreciation is a tax incentive designed to stimulate business investment by allowing investors to accelerate the depreciation of qualifying assets, such as equipment, rather than write them off over the useful life of the asset. This strategy can reduce a company's income tax, which in turn reduces its tax liability.

Medical professionals can claim accelerated bonus depreciation as a limited partner when investing passively into a real estate syndication. As a limited partner (LP) passive investor, you get a share of the returns based on how much you invest.

Similarly, you get a share of the tax benefits as well, as documented by the Schedule K-1 you would receive each year. The K-1 shows your income for a particular asset. In many cases, particularly in the first year of the investment, that K-1 can show a loss instead of an income.

The magic of the K-1 is that it includes accelerated and bonus depreciation. In other words, even while you’re receiving cash flow distributions, the K-1 can show a paper loss, which in most cases means you can defer or reduce taxes owed on the cash flow you’ve received.

Cash Flow Deals

These deals don't offer tax benefits, but can generate so much income that they outperform potential tax savings. Investments in this category include things like algorithmic trading. You can invest in cash flow deals through a tax shelter, such as your Private Foundation, to get the initial tax savings as well as tax advantaged portfolio growth.

Legal Strategies For Medical Professionals

Estate planning is something everybody needs to do at some point. Lawsuits can happen to anyone, and high-net-worth medical professionals are especially at risk. All it takes is a car accident, an injury on your property, a contractual disagreement—and once somebody knows what you own, they can hire a good attorney to force you to settle out of court.

The way you protect yourself is to set up asset protection. Holding companies can shield anything of value, such as real estate properties and investments. Operating companies can be established for business activities like collecting rent, paying contractors, and signing contracts.

Trusts are a way to guarantee anonymity across all of your entities and assets. They allow you to look like a beggar on paper and transfer your assets anonymously to your heirs, taking the target off your back.

Here are a couple of other legal structures we help our clients set up:

S Corporations

Independent doctors or physicians can create S Corporations to handle their taxes. Unlike regular corporations (where profits get taxed twice), S corporations pass their income, losses, and deductions directly to their owners. An S Corp, or S corporation, is a “pass-through” entity, which means that the profits and losses of the business are passed through to the individual owners and are taxed at the owners’ personal income tax rates.

Instead of paying corporate taxes, each owner reports their share of the business’s money on their personal tax returns, paying taxes at their individual rates.

Solo 401(K)

What about retirement?

If you are a medical practitioner who works as an independent contractor, The Solo 401(k) is an ideal retirement plan because it lowers your taxable income and enables you to build up retirement funds through high contribution limits and almost limitless investment capability.

The Solo 401(k) is a qualified retirement plan, just like hospital-sponsored plans. You can contribute to the plan on a tax-deferred basis. You can also contribute Roth funds to the plan and invest tax-free. With some of the highest contribution limits, the Solo 401(K) lets medical professionals lower their taxable income and grow their retirement quickly.

To Wrap It Up …

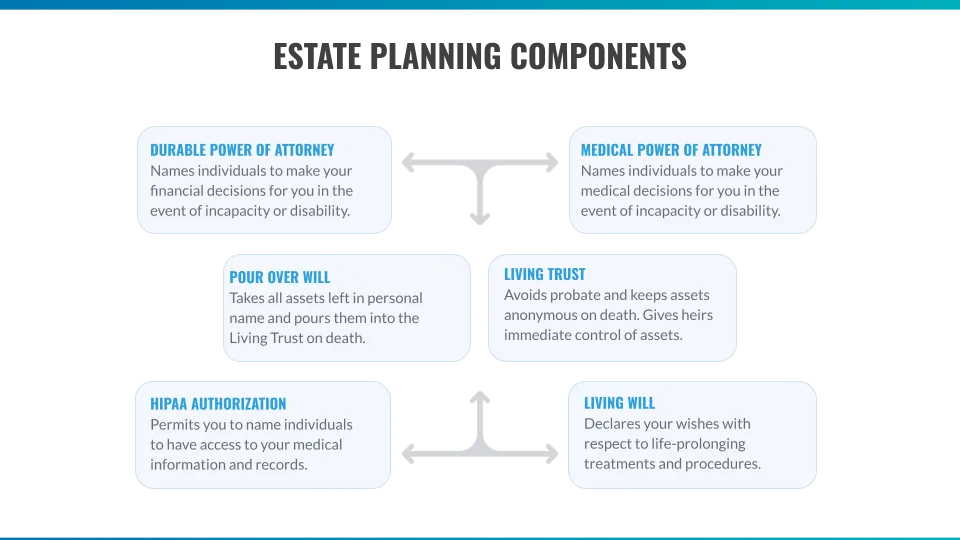

Even medical professionals with no investments need entity structuring. Here is what a full legal diagram could look like, which includes asset protection structures, estate planning, and tax shelters.

As you accelerate your tax and investing approach, it's important to add in measures to prevent a catastrophic reset. We can show you how to save $20k or more in taxes during the first year, but you will want to set up additional tax and legal structures over time to continue to reduce your taxes down to the 0-10% range.

Without entities, this would be impossible.

It's also important to protect yourself from catastrophic events, no matter how unlikely, so that you don't have any major setbacks on your journey to time and financial freedom.

Tax, Investing, and Legal Strategies for Tech Professionals

Tech industry professionals thrive on innovation, cutting-edge technology, and rapid growth.

However, navigating the world of personal finance requires a different set of skills.

Whether they're W2 employees or entrepreneurs, experienced tech professionals can earn lucrative compensation packages, which unfortunately means significant tax liabilities. That’s why they have to optimize tax strategies and get professional help navigating complex tax laws.

Or if they own a business or have exited a business, our capital gains page can help (if they made a ton of money in their exit and are looking for tax strategies to offset that).

The unique financial challenges faced by tech workers call for tailored tax, investing and legal strategies to help you make the most of your wealth. These include:

Navigating the world of taxes can be daunting, especially for tech workers with complex compensation packages, stock options, and freelance gigs. With the right strategies, however, you can make an informed decision about the best steps to take to secure your financial future.

Let’s get started.

Tax Planning for Tech Professionals

Equity compensation, a high income, remote work (where your employer is in another state with different laws) … These can make tax planning for tech professionals quite complex.

You have to take a lot into account.

Different types of equity compensation have different tax treatments. For example, Restricted Stock Units (RSUs) are taxed as ordinary income upon vesting. Incentive Stock Options (ISOs) may qualify for preferential tax treatment if certain holding periods are met. Non-Qualified Stock Options (NSOs) are taxed as ordinary income upon exercise. But exercising ISOs can trigger Alternative Minimum Tax (AMT) liability.

Lost yet? It can get pretty confusing very quickly.

I believe a solid wealth management strategy starts with tax planning. Remember: salaried (full-time) tech workers are taxed on gross income first, with the IRS taking their cut before you receive your paycheck.

Compare this to business owners and investors (with the correct structures in place), who pay the IRS quarterly on their net income after expenses.

When you (as a full-time employee) invest through a properly structured entity, your investment income gets the same tax treatment as a business. This allows you to use your money before deducting taxes.

Tech professionals early in their careers may benefit from Roth conversion strategies, paying taxes now on traditional retirement accounts to enjoy tax-free growth and withdrawals in the future. This isn't nearly as strong as the foundation or depreciation deals, however.

But if you’re like most of our clients, you’re further along in your career, making a good salary, and you've been told there isn't much you can do to lower your taxes beyond taking deductions or using retirement vehicles like 401ks and IRAs.

High earners in the tech field spend years growing their career and growing their income. The more they make, the more it hurts to see 20-30% of earnings yanked away by the IRS.

I have good news for you: The right CPA can show you how to layer tax strategies to dramatically cut your taxes and even reach the 0-10% range, depending on how aggressive you decide to go.

(Here's the catch: To achieve 0-10%, you actually have to implement all the tax strategies. That's like eating your veggies, nobody wants to do it.)

Many CPAs don’t understand that it's possible to save outside the standard deductions. Things like tax-loss harvesting can offset gains and reduce tax liability. Charitable giving or even setting up a private nonprofit foundation can also help.

A high-level CPA will be able to help you navigate complex tax decisions and make it seem easy. They can find creative (but completely legal) ways to save taxes. And that savings can be invested in equally creative, equally overlooked ways.

Such as …

Investing Strategies For Tech Professionals

After implementing all the best tax strategies, our tech clients then focus on investing their tax savings into tax-advantaged deals. There are tons of deal types, but there are two categories of investments you really need to know about:

W2 earners should invest in energy or machinery deals that allow them to be a general partner (GP) in the first year in order to claim accelerated bonus depreciation. As of this writing (December 2024), syndications have changed over the past year. They only way to get depreciation as a W2 is to be a GENERAL PARTNER (not LIMITED). This only works for ENERGY & MACHINERY. RV PARKS would require you to be a Real Estate Professional.

If you are a Real Estate Professional, you can also access bonus depreciation from multi-family and commercial investments.

Cash flow deals deals don't offer tax benefits, but can drive so much income that they outperform the tax savings. Investments in this category include things like algorithmic trading and small business funds. One of the top strategies is to invest in cash flow deals through a tax shelter, such as a 501(C)3 Non-Profit Private Foundation, to get the initial tax savings as well as tax advantaged portfolio growth.

Tech pros need to know about e three "financial freedom" strategies they can avail themself of:

Save on taxes (typically this year)

Generate more cash flow (typically this year)

Create a nest egg so you can retire as fast as possible

The first two are short-term strategies. You can save taxes with Royal Legal's tax strategies (and you may still use a foundation, but only as one of many tools to capture tax savings) and you can generate cash flow with something like algorithmic trading.

Creating a nest egg requires a longer-term strategy. Putting money into your own foundation, THEN investing in cash flow deals is the strongest possible move—as long as you don't want to have a bunch of cash on hand. Because once it's in the Foundation, it's no longer yours. We endorse this strategy because that's the best possible move for anybody interested in achieving financial freedom.

Legal Strategies For Tech Professionals

Software executives, Saas founders, and other tech professionals have giant targets on their back when it comes to frivolous lawsuits.

All it takes is a car accident, an injury on your property, or a contractual disagreement—and once somebody knows what you own, they can hire a good attorney to pressure you until you settle out of court.

The way you prevent this is to set up asset protection before you get sued.

Anonymity across all of your entities and assets is key. Holding companies are where you should place your assets. This could be things like real estate properties or other investments. Anything of value that could be exposed during a lawsuit is important to protect. Operating companies run everything.

So here's what you'll be doing:

#1. Set Up a Holding Company

This is what "holds assets," typically anonymously. There are three kinds:

Series LLC

Delaware Statutory Trust

Hub-And-Spoke / LLC (most recognizable as the Wyoming LLC)

#3. Set Up an Operating Company

This is what does your "operations." Collecting rent, paying bills, performing key functions and transactions. This is what turns into the S-Corp because the money is flowing through (but not held inside for very long) this entity, which allows us to apply tax strategies to it.

In this case, you are mixing both. So you would want to differentiate…

Entity structuring means creating LLCs so your assets are held anonymously and separate from your high risk business transactions. We recommend a holding company for any investments or assets. Then a separate operating company for business transactions, such as your consulting side gig. When the operating company reaches $75k/year income, you should turn it into an S-Corp. etc…

PS - The $75k range (sometimes as low as $50k) is basically where you start to save money on taxes.

The reason it takes until then is that the S-Corporation requires a separate tax return and payroll, which both cost money in the $1-2k range. So it doesn't really pay for itself until a certain income threshold.

Unlike C Corps (that face corporate taxes and then shareholder taxes on dividends), S Corps allow shareholders to pay taxes only at their individual income tax rates, simplifying the process. S Corps split profits into wages and distributive shares, the latter of which is not subject to self-employment taxes. This distinction can provide considerable savings on the Social Security and Medicare tax burden.

We’ll also help you employ different types of trusts to create anonymity at the County Recorder and Secretary of State offices, as well as during probate (so you look like a beggar on paper and can transfer your assets anonymously to your heirs).

My team can show you how to save $20k or more in taxes during the first year, and additional tax and legal structures will continue to reduce your taxes down to the 0-10% range. Without entities, this would be impossible.

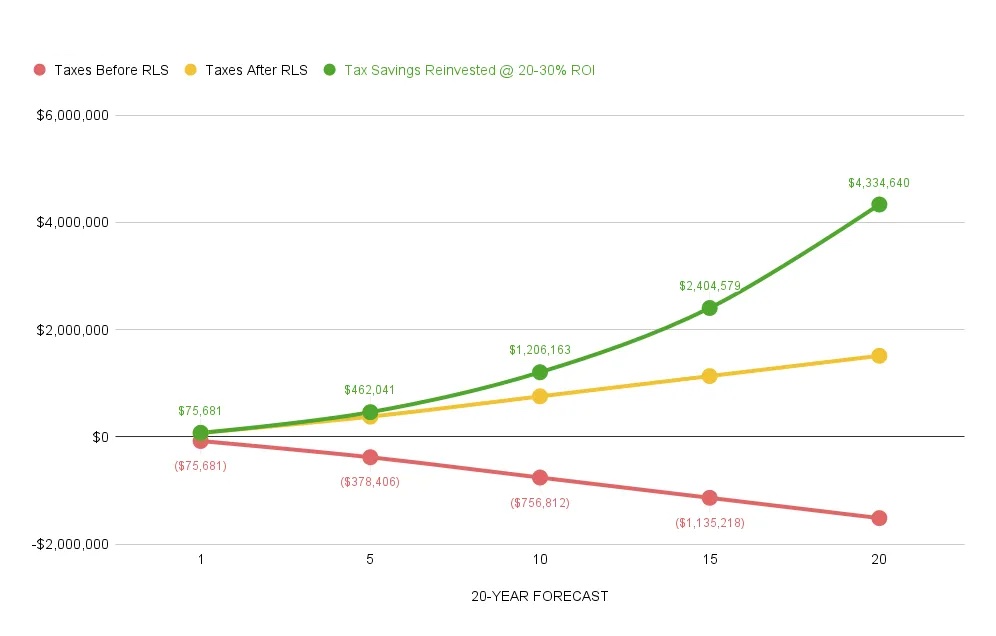

Here’s a 20-year forecast that shows how the right combination of tax strategies, investing and corporate entity structure can grow your wealth:

Protect yourself from lawsuits with estate planning, no matter how unlikely you think they are, so that you don't have any major setbacks on your journey to time and financial freedom.

The Path From High Tech To Financial Freedom

You’ve worked hard your entire life. It’s time to gain control over your time and money. Rapidly achieving true freedom requires a good tax and investment strategy.

We help tech executives and other professionals in the digital space save $20k or more in taxes during the first year—then re-invest that tax savings into turnkey properties, ATMs, self-storage syndications, apartment complex rehabs and more. We help them create the right tax and legal structures to continue to reduce your taxes and create true anonymity to protect their money.

In the end, we can help you:

Own assets anonymously so that your wealth isn't at risk

Set up limited liability companies to protect your wealth from lawsuits

Minimize risk by separating your business activities from your assets

Hold each asset in isolation so that lawsuits can't jeopardize your entire portfolio

Use insurance as a last line of defense

Tax, Investing, and Legal Strategies for W2 Employees

Not-so-fun fact: As a W2 employee, you are taxed at a rate higher than businesses and investors.

In fact, no group in America pays more taxes than high-salary wage-earning W2 employees.

Whether you are a medical professional, a tech professional or any other full-time employee for a U.S. company, there are some little-known ways you can jumpstart your tax savings and investment journey.

Let’s take a look at these tax, investing and legal strategies for 9-to-5’ers so you can make an informed decision about the best steps to take to secure your financial future.

Tax Strategies for W2 Employees

Tax planning is a key component of a solid wealth management strategy. Remember: W2 employees are taxed on gross income first, with the IRS taking a portion before you receive your paycheck.

In contrast, business owners and investors (with the correct structures in place) pay the IRS quarterly on their net income after expenses.

When you (as a full-time employee) invest through a properly structured entity, your investment income gets the same tax treatment as a business. This allows you to use your money before deducting taxes.

If you’re like most of our clients, you've been told there isn't much you can do to lower your taxes beyond taking deductions or using retirement vehicles like 401ks and IRAs. That’s why finding the right CPA to work with is so crucial. You need someone who knows what they’re talking about.

The right CPA can help W2 earners leverage tax strategies to achieve and maintain tax rates in the 0-10% range. This accelerates your overall cash flow and net worth.

Many CPAs don’t understand that it's possible to save outside the standard deductions. A high-level CPA is someone who earns a high income themselves, someone who has personally found a way to pay nearly $0 in tax by leveraging advanced strategies.

If you find a CPA with an MBA and who can perform Chief Financial Officer functions, even better— these folks will be able to help you navigate complex tax decisions and make it seem easy.

When you work with that level of CPA, you'll start to find creative (but completely legal) ways to save taxes. And that savings can be invested in equally creative, equally overlooked ways.

Such as …

Investing Strategies For W2 Employees

W2 employees spend years growing their career and growing their income. At a certain point we have plenty of income but 20-30 percent of it is being sucked away by the IRS.

Saving money on tax is important, but the real magic happens once W2 earners invest their tax savings into tax-advantaged deals.

There are tons of deal types, but the top asset classes include real estate, syndications in energy or machinery, and algorithmic trading. In short, deals can do three things:

Give you ROI (for example, after 3 years, you get twice your money back)

Give you cash flow (ex: you get dividends/distributions every quarter)

W2 earners should invest in energy or machinery deals that allow them to be a general partner (GP) in the first year in order to claim accelerated bonus depreciation. As of this writing (December 2024), syndications have changed over the past year. They only way to get depreciation as a W2 is to be a GENERAL PARTNER (not LIMITED). This only works for ENERGY & MACHINERY. RV PARKS would require you to be a Real Estate Professional.

If you are a Real Estate Professional, you can also access bonus depreciation from multi-family and commercial investments.

Cash Flow Deals

These deals don't offer tax benefits, but can drive so much income that they outperform the tax savings. Investments in this category include things like:

Algorithmic trading (ex: Forex)

Small business funds

A variety of deals that call themselves cash flow, meaning they focus on providing you with cash right away.

One of the top strategies is to invest in cash flow deals through a tax shelter, such as a 501(C)3 Non-Profit Private Foundation, to get the initial tax savings as well as tax advantaged portfolio growth.

You see, there are three "financial freedom" strategies at a high level:

Save on taxes (typically this year)

Generate more cash flow (typically this year)

Create a nest egg so you can retire as fast as possible

#1 and #2 are short-term strategies. You can accomplish #1 with Royal Legal's tax strategies (and you may still use a foundation, but only as one of many tools to capture tax savings) and you can accomplish #2 with a good cash flow deal (algorithmic trading, for example).

#3 is a longer-term strategy. Putting money into your own foundation, THEN investing in cash flow deals is the strongest possible move—as long as you don't want to have a bunch of cash on hand. Because once it's in the Foundation, it's no longer yours.

So when we endorse this strategy, it's because that's the best possible move for anybody interested in #3 - achieving financial freedom.

Legal Strategies For W2 Employees

As you accelerate your tax and investment approach, it's important to incorporate asset protection and legal strategies into your plan. The Royal Legal approach for W2 earners lets you:

Own assets anonymously so that your wealth isn't on public display

Set up limited liability companies to protect your personal net worth from lawsuits

Minimize risk by separating your business activities from your assets

Hold each asset in isolation so that lawsuits can't jeopardize your entire portfolio

Use insurance as a last line of defense in case everything goes wrong

Even a W2 employee with no investments needs to set up legal support. Everybody needs an estate plan, not just for their kids but also in case they become incapacitated and need someone to help make medical and financial decisions (ex: car accident, COVID, etc...).

Setting up an LLC, even as a small consulting or investing firm, can give you options to a big range of new strategies.

Once your LLC hits the $50-75k income mark, the S-Corp election becomes your best friend. S Corps utilize pass-through taxation, meaning income and losses "pass through" the company directly to the shareholders.

Unlike C Corps (which have corporate taxes and then shareholder taxes on dividends), S Corps allow shareholders to pay taxes only at their individual income tax rates, simplifying the process.

For businesses generating between $75,000 and $250,000 in profits per owner, electing S-Corp status can offer significant savings. While LLCs face self-employment taxes on all profits, S-Corps split profits into wages and distributive shares, the latter of which is not subject to self-employment taxes. This distinction can provide considerable savings on the Social Security and Medicare tax burden.

The S Corps elections also means you can write off business expenses such as equipment, work meals, travel and more. For example, you can depreciate vehicles—80% if under 6,000 lbs or 100% if over 6,000 lbs.

You can even pay your kids to work, typically up to around $14k/year. They avoid income tax and you avoid having profit taxed at your normal income tax rate. Win/win!

There’s a Path to True Financial Freedom For W2 Employees

You’ve worked hard your entire life. It’s time to gain control over your time and money. Rapidly achieving true freedom requires a good tax and investment strategy.

We can show full-time, W2 workers how to save $20k or more in taxes during the first year. Then we give you access to high performance deals and model out different investment options so you can see the best path to rapidly achieve your financial goals.

The Private Foundation. Oil & gas syndications. Machinery deals. And short-term rentals. These are your best options as a W2. The list of deals that outperform traditional stock market investments (and sometimes provide additional tax benefits) is long.

Take a look at a typical 20-year plan that includes asset protection structures, estate planning, investing and tax shelters:

Kamala Harris Capital Gains Tax: Changes To Expect (Jan. 2025 Update: Well, That Didn't Happen!)

Jan. 2025 Update: Well, the U.S. Election went the other way. Whatever your feelings about it, here are some things to expect from the incoming Trump administration regarding capital gains:

Donald Trump wants to make the tax cuts in his 2017 tax law permanent and lower federal income tax rates for individuals. Trump hasn't said much about long-term capital gains tax, although he floated the idea of a temporary capital-gains tax holiday.

Project 2025, designed for the next Republican administration and spearheaded by the Heritage Foundation, suggests two changes to the capital gains tax. First, the plan calls for a 15% top long-term capital gains tax rate, down from 20% now.

Project 2025 supports the idea of indexing capital gains for inflation each year, meaning taxpayers would be able to increase their tax basis in capital assets by the rate of inflation between the purchase date and time of sale.

Here's an example from Kiplinger: If you bought stock in 2010 for $10,000 and sold it in January 2024 for $35,000, you would have a $25,000 long-term capital gain ($35,000 - $10,000).