Selling an Inherited House With Siblings? Here's What To Know

Are you selling an inherited house with your siblings?

Dealing with the death of a parent or guardian is already tough, but the administrative and legal tasks that go hand-in-hand with settling their estate can make it tougher. If you're inheriting a house with siblings, there are also financial and sentimental challenges to navigate—especially if your brother or sister refuses to sell or has other ideas for the property.

What your loved one intended to be a gift can become a burden if this process isn't handled properly. That's why families opt for selling an inherited home as-is to minimize the timeline and see the financial returns as soon as possible.

Types of Home Inheritances

Inheriting a home may seem pretty straightforward. However, different types of inheritances can impact how you handle the sale of the property: deed inheritance, will inheritance, and trust inheritance.

A deed inheritance works similarly to a life insurance policy. Also known as a "Title by Contract," this applies to mortgages that have a beneficiary or beneficiaries listed to receive the property in the event of the contract holder's death. The beneficiary is listed as a "remainderman." A remainderman is a person who inherits or is entitled to inherit the principle of a trust once it is dissolved.

A will inheritance is a bit more complicated to manage. This type of home inheritance is what most people envision when they consider an inheritance. The property owner leaves the house to you and your siblings in the will. However, as the will is not a part of the original ownership contract, you must use the will to go through probate proceedings to secure the property. This process delays the sale of the home by months.

Finally, a trust inheritance indicates that you and your siblings are entitled to the home after a certain age. This type of inheritance typically doesn't apply to adult children or siblings.

Determining the type of inheritance you've received will help you understand the timelines and legalities involved. It's worth hiring an attorney to navigate these processes.

Selling an Inherited House? Understanding Inherited Ownership

When you inherit a house with your siblings, state law dictates that you share ownership equally. In addition to sharing the asset, you're also equally responsible for any outstanding liabilities and debts (i.e., the mortgage and property taxes) and for claiming income from the property.

This means that you and your siblings will be equally responsible for paying debts— especially if there's no life insurance to cover the outstanding mortgage— even if you have different income levels. Additionally, you'll all have taxable income from the sale to navigate with the IRS. It's worth getting professional legal and accounting advice as individuals when navigating the process.

It's also important to note that selling an inherited house can't take place without agreement from all of the listed beneficiaries. If a sibling is pushing back, you may require legal intervention before listing the home.

It should be no surprise that handling the administration of dividing debts and income and listing the home is a significant undertaking. If one sibling handles the majority of the work, they are legally entitled to additional compensation for their time from the estate. Again, having legal counsel in place to assist is beneficial.

Dealing with an Outstanding Mortgage

Getting mortgage insurance is one of the best things a homeowner can do to protect their family should death occur— unfortunately, many opt out of this coverage. When mortgage protection is in place, the costs are covered, and the beneficiaries don't have to worry about paying it off.

So what about those cases when the parent didn't have mortgage insurance or life insurance, and a mortgage is still outstanding?

Rest assured that under federal law, a mortgage lender cannot demand the entire mortgage in a lump sum from the beneficiaries of inheritance. In some states, there are even protections in place to give beneficiaries the right to walk away from an inheritance with a mortgage without the bank being able to go after their personal assets.

The process of transferring a mortgage after death is contingent on each lender's policies and procedures. Generally, it's a lot of tedious paperwork, but not too difficult. Inheriting a mortgage does mean you'll be required to make those payments until the house is sold. When the home sells, the profits will be applied to paying off the mortgage before being divided between the beneficiaries.

Home Inheritance Taxes

When you inherit a home, a policy called "stepped-up basis" comes into effect. This policy ensures you only pay gains on the selling profit versus the home's value today rather than the original value. Suppose your parents bought the home for $50,000, and it's now worth $200,000. You sell it as-is for $220,000. You and your siblings would be taxed on the gains of $20,000 rather than $170,000.

It's important to understand this concept, as many parents mistakenly "gift" the home to their children before their death. In that case, you would be taxed for the $170,000 gain.

Selling a House As-Is

Selling an inherited house as-is means that you're listing the property in its current state with the understanding among buyers that you won't be making any repairs. Buyers still retain the right to have an inspection completed, negotiate the price, and access a full property disclosure from the sellers.

The advantage of selling a house as-is is that you won't have to put any time and money into the property before selling. This streamlines the process of paying off the mortgage, potentially getting extra money, and moving on with your lives.

As inheriting a home with siblings can be complex, it's important to hire a professional attorney and consult with a skilled accountant.

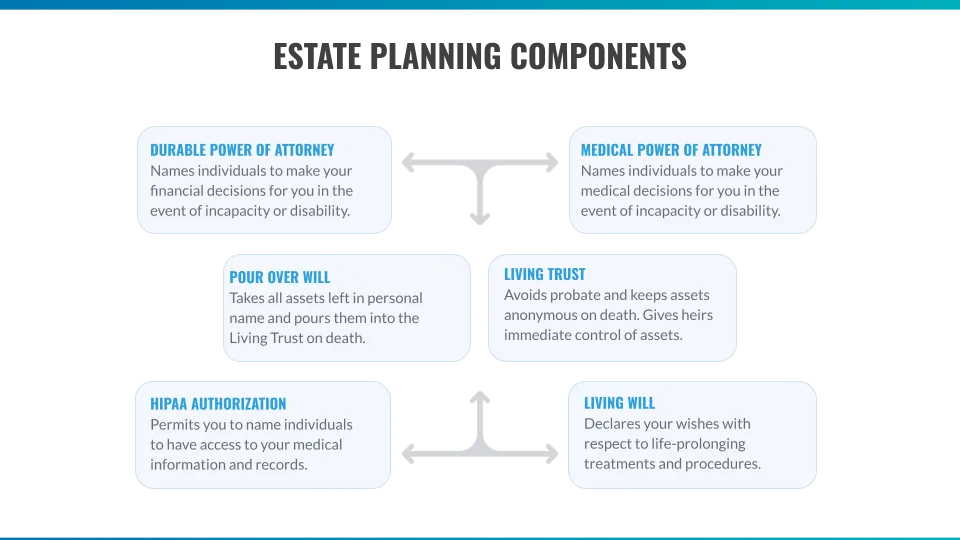

Key Takeaway

Spare loved ones the pain of probate and ensure that your assets are distributed exactly according to your wishes by having a professional estate plan put in place. This can be accomplished through a 3-part strategy that involves a Living Trust, Pour Over Will, and power of attornies for making medical, financial, and managerial decisions. By not having a proper estate plan, you are at extreme risk of losing up to 1/3 or more of your estate to probate court and attorney fees. To learn more about Royal Legal Solution's rock-solid estate plan service, visit Estate Planning for Real Estate Investors.